Bill Ackman and Michael Burry think so

TLDR

Fannie and Freddie are back in focus, and we’re long. The thesis is that Fannie Mae will eventually exit conservatorship via IPO, driven by capital accumulation and increasing political pressure. Timing remains uncertain given legislative and regulatory risk, but that uncertainty is offset by Fannie’s position as part of a government-backed duopoly that guarantees ~25% of the U.S. mortgage market. The business generates $14–17B of annual net income, and as capital continues to build, pressure to resolve conservatorship will increase. While near-term catalysts are uncertain, we believe an IPO is likely over time; in the meantime, we are comfortable owning a high-quality business as the situation develops.

Intro

We are not attempting to reinvent the wheel. Fannie Mae has been extensively analyzed across research reports, litigation, legislation, and market commentary.

The complexity of this opportunity does not lie in building a traditional valuation model. Rather, it lies in synthesizing a wide range of non-traditional drivers - political incentives, legal outcomes, and regulatory decisions - that ultimately determine the path forward.

The goal of this piece is to distill that complexity into a coherent framework, summarizing the existing landscape and presenting a clear, actionable view of the risks and potential upside.

The big names, Ackman & Burry, are weighing in on Fannie Mae. This isn’t going to be for the faint of heart. Investing is hard. Politics is unpredictable. This opportunity sits at the intersection of both. Warren Buffet quips that investing is a game of baseball but no one is calling strikes so you should wait for your pitch. This is an easy one to sit out. For everyone else that wants to take a swing: let’s ride.

Before we get excited, this is potentially a very long play. It’s hard to put enough emphasis on long. Ackman first entered this trade in 2013. He was talking about Fannie Mae back on Charlie Rose in 2008. He was on Charlie Rose again in 2015 pitching why Fannie should be public. His patience is legendary and needs to be studied.

I wouldn’t take Ackman’s word at face value though. Never forget his famous covid trade where he warned ‘hell is coming’ because of covid: he then pocketed $2B in bets against markets**.**The world is full of beauty. The art world has the Mona Lisa, math has the Fibonacci Sequence, computer science has the illusion of multitasking, and in finance we have Bill Ackman’s covid trade. Beauty aside, let’s dig in.

Fannie giveth and she taketh. If you were invested pre 2008, good riddance. If you effectively bet on the election in ‘24, then congratulations, that bet paid off nicely (yes, that would have been a bet, not investing).

History & Conservatorship Timeline

Fannie Mae was created in 1938 by Roosevelt to ease the housing crisis that resulted from the Great Depression. If you want to dig into the history more deeply you can find good summaries here, here, here, and here.

2008

A quick summary from authoritative sources.

“On September 6, 2008, with the consent of both Fannie Mae's and Freddie Mac's (the Enterprises) boards of directors, the Director of FHFA exercised statutory authority to place each Enterprise into conservatorship. This established the two conservatorships in response to a substantial deterioration in the housing markets that severely damaged each Enterprise's financial condition and left both of them unable to fulfill their missions without government intervention.” - FHFA.gov

“Fannie Mae and Freddie Mac continue to operate under conservatorship, as they have since 2008. The U.S. Department of the Treasury (Treasury) provides Fannie Mae and Freddie Mac with financial support through the Senior Preferred Stock Purchase Agreements (SPSPAs), which were executed on September 7, 2008.

The SPSPAs were designed to ensure that Fannie Mae and Freddie Mac, respectively: (i) provide stability to the financial markets; (ii) prevent disruptions in the availability of mortgage finance; and (iii) protect the taxpayer.

In exchange for Treasury’s financial support, the SPSPAs require Fannie Mae and Freddie Mac, among other things, to make quarterly dividend[emphasis ours] payments to Treasury, provide Treasury with a Liquidation Preference, and beginning in 2010 pay Treasury a periodic commitment fee that reflects the market value of the outstanding Treasury commitment, as well as Stock Warrants for the purchase of common stock representing 79.9% of the common stock of Fannie Mae and Freddie Mac, respectively, on a diluted basis.” - FHFA.gov

`

The Conservatorship

“In order to restore the balance between safety and soundness and mission, FHFA has placed Fannie Mae and Freddie Mac into conservatorship. That is a statutory process designed to stabilize a troubled institution with the objective of returning the entities to normal business operations[emphasis ours]. FHFA will act as the conservator to operate the Enterprises until they are stabilized.” - James Lockhart, FHFA Director, 9/7/2008.

That was almost 20 years ago though. What happened since then? Here’s the timeline:

- **The Original Bailout (September 7, 2008):**the U.S. Department of the Treasury provides Fannie Mae and Freddie Mac with financial support through the Senior Preferred Stock Purchase Agreements (SPSPAs)

- First amendment (May 6, 2009): Treasury increases the commitment of financial support from 200 million respectively.

- **Fannie can’t pay dividends from earnings (2008 - 2012): “**Rather than use 10% (or in some cases 12%) of the liquidation preference to calculate the Dividend Amounts - a practice which was contributing to the Enterprises need to draw on Treasury’s commitment of financial support - the Third Amendment based the Dividend Amounts on the Enterprises’ net worth. This helped ensure the Enterprises’ financial stability, fully captured financial benefits for taxpayers, and eliminated the need for Fannie Mae and Freddie Mac to circularly borrow from Treasury only then to pay dividends back to Treasury.” (source)

- **Third amendment (August 17, 2012):**Treasury amends the agreement to effectively sweep 100% of Fannie Mae’s earnings to the Treasury.

- Fannie technically was able to pay 12% PIK but the government didn’t pursue that option and instead created this amendment that sweeps all profits, effectively preventing Fannie from ever recapitalizing.

- Fourth amendment (April 13, 2021): the Preferred Stock Purchase Agreements (PSPAs) is amended to enable Fannie Mae to retain additional earnings in excess of the 25 billion. (source)

- January 2, 2025, the Treasury Secretary and FHFA Director of the outgoing administration further amended the PSPAs. The amendment restored Treasury’s right to consent to a release from conservatorship, which it had previously from 2008 to 2021. Practically, Treasury always had this right, as exiting conservatorship is not possible without addressing Treasury’s Senior Preferred Stock.

- September 7, 2028 - Treasury expects that the parties will agree in the future to extend the September 7, 2028, expiration date to the extent appropriate in order to avoid any possibility of a disorderly or disruptive exit from conservatorship.

A brief legal aside

From 2008 - 2011, Fannie Mae couldn’t pay their dividends so they borrowed money from the Treasury to pay the dividends. It was a circular borrowing loop. However, they never exercised their 12% PIK option which was outlined in their first amendment.

“For each Dividend Period from the date of the initial issuance of the Senior Preferred Stock through and including December 31, 2012, “Dividend Rate” means 10.0%; provided, however, that if at any time the Company shall have for any reason failed to pay dividends in cash in a timely manner as required by this Certificate, then immediately following such failure and for all Dividend Periods thereafter until the Dividend Period following the date on which the Company shall have paid in cash full cumulative dividends (including any unpaid dividends added to the Liquidation Preference pursuant to Section 8) the “Dividend Rate” shall mean 12.0%.” -

The cash sweep is outlined in the third amendment here: “the ‘Dividend Amount’ for a Dividend Period means the amount, if any, by which the Net Worth Amount at the end of the immediately preceding fiscal quarter, less the Applicable Capital Reserve Amount, exceeds zero”.

The legal basis and economic justification for this is questionable. The 12% PIK option provided a mechanism for the Enterprises to pay their dividends. A 100% cash sweep is aggressive and laid the foundation for the government to generate significant profits on the Fannie Mae bailout, unlike bailouts of other companies.

Once the government passes the amendment to sweep 100% of profits, it’s not clear how Fannie Mae ever exits it’s conservatorship. The fourth amendment in 2021, 13 years after the original conservatorship, enabled Fannie Mae to recapitalize with $25 billion in reserves. That’s a step in the right direction towards exiting the conservatorship.

Legal Action

A town with one lawyer has a starving lawyer. A town with two lawyers has two rich ones.

There are two legal cases to summarize: i) Collins v. Yellen and ii) a class action lawsuit by shareholders

Collins v. Yellen

This case encapsulates two issues and multiple claims.

Issues

-

Can the President fire the FHFA director without cause?

-

Did the cash flow sweep exceed FHFA authority?

Outcome

“In a two-part decision, the Supreme Court ruled that the restriction on removal of the FHFA director by the President was unconstitutional in light of Seila Law, and secondly, dismissed the lawsuit brought against the FHFA by shareholders of Fannie Mae and Freddie Mac as the takeover of these firms was an established power of the agency under terms of the Housing and Economic Recovery Act of 2008.” - Collins v. Yellen

On the day of this decision, June 23, 2021, Biden fired Mark Calabria, the FHFA director who was appointed under Trump and supported Fannie going private. Unsurprisingly, there’s political tension here.

Class Action Litigations

Issue:

Was the cash flow sweep legal? This is from the perspective of a breach of the implied covenant inherent in shareholders’ contractual relationships with Fannie Mae and Freddie Mac.

Outcome (ongoing)

“Trial in this litigation was held between July 24, 2023 and August 14, 2023. The trial resulted in a jury verdict in favor of the Plaintiffs. On March 14, 2025, the Court denied Defendants’ post-trial Motion for Judgment as a Matter of Law. The litigation is currently under appellate review, with oral argument scheduled for Tuesday, April 21, 2026 at 9:30am before a three-judge panel of the U.S. Court of Appeals for the District of Columbia Circuit. Further updates will be provided on this website as they become available.” fannie-freddieclassaction.com

Takeaways

Litigation has mostly been unfavorable to shareholders. That’s not a terrible thing per se - if it was favorable then this wouldn’t be an issue anymore. The class action lawsuit is ongoing and oral arguments start on April 21st. We’ll watch this closely.

Valuation

Business Model

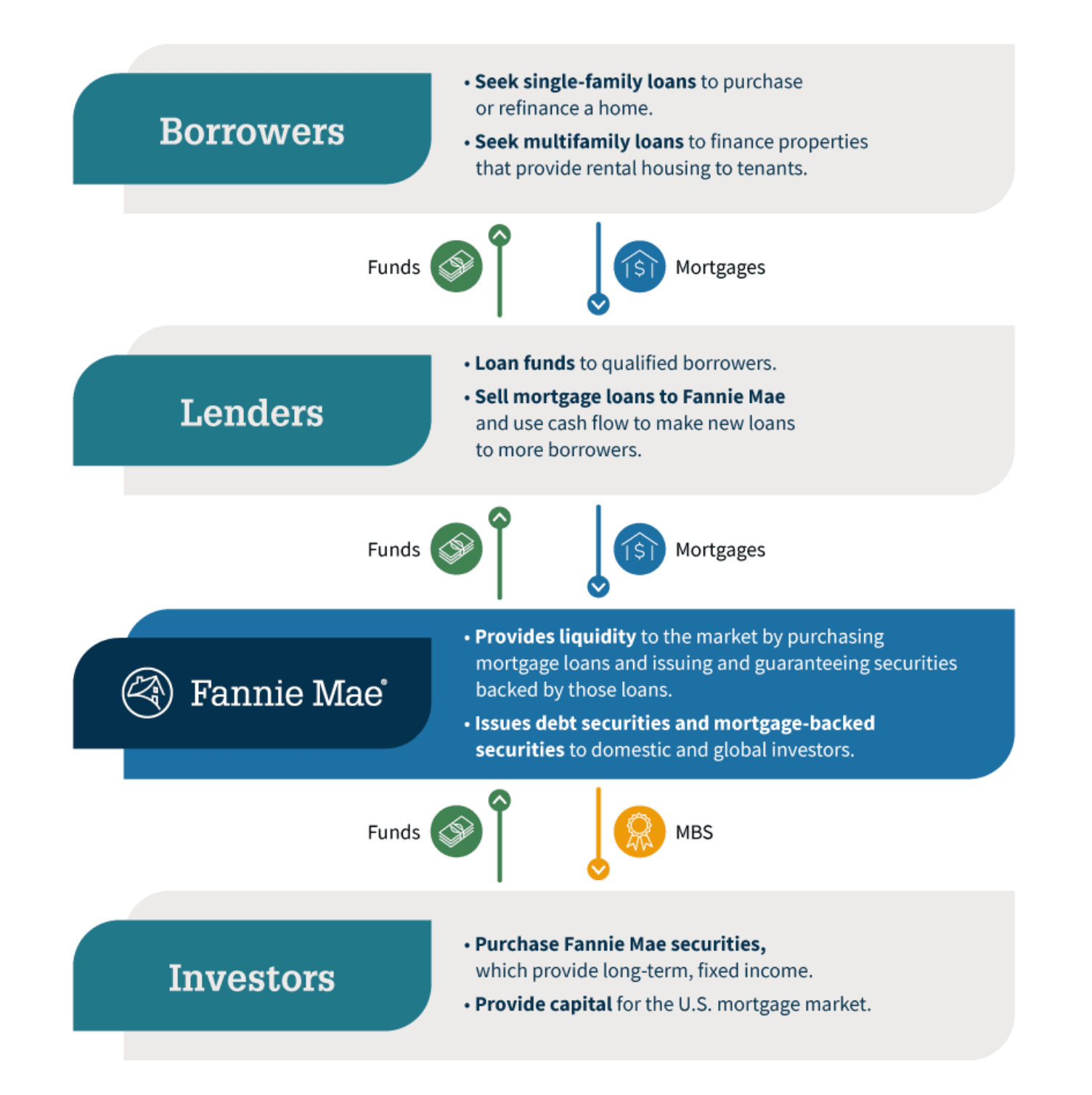

Fannie Mae purchases mortgages and securitizes them into mortgage-backed securities (MBS), which are sold to investors as fixed income. MBS investors know they will receive timely payment of principal and interest, because of the Fannie Mae guarantee. Fannie Mae earns a guaranty fee for assuming the credit risk on loans underlying the MBS.

This diagram outlines the funds flow from borrowers → lenders → Fannie Mae → Investors.

Comps

We can think of Fannie as a utility or an insurance company (probably closer to a reinsurer due to the sheer scale).

*Utility Model:*Fannie functions like a financial utility by providing standardized, reliable infrastructure for the U.S. mortgage market, ensuring continuous liquidity for 30-year fixed-rate loans regardless of market conditions. It operates at massive scale with regulated returns and public policy objectives, similar to Duke Energy or American Water Works, which deliver essential services.

Its guarantee business is analogous to toll collection on a national housing network, earning a small, recurring fee on trillions of mortgages. Barriers to entry are extremely high due to regulation, standardization, and its central role in mortgage securitization, making competition effectively nonexistent. As a result, Fannie exhibits utility-like characteristics: stable demand, predictable cash flows, and system-critical importance.

*Credit Guarantor:*Fannie operates primarily as a credit guarantor: it guarantees principal and interest on mortgage-backed securities (MBS) and earns a guarantee fee (~50–65 bps) for taking borrower default risk. Investors in Fannie MBS bear interest rate and prepayment risk, but not credit risk—Fannie absorbs losses if borrowers default. Unlike banks, Fannie does not rely on earning a lending spread; its core economics come from pricing and managing credit risk across a $4T+ guaranteed book.

G-Fees

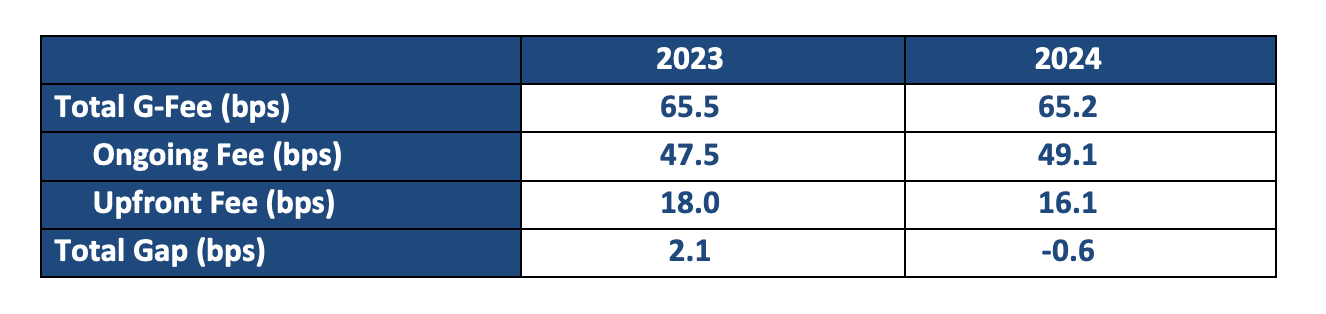

Fannie Mae retains a guarantor fee (the G-fee) from the payments received on mortgages as compensation for guaranteeing the timely payment of principal and interest on the mortgage pass-through securities (source). The G-fee, covers projected credit losses from borrower defaults over the life of the loans, administrative costs, and a return on capital (FHFA).

The FHFA does annual studies on the G-Fee and breaks it down by multiple dimensions (e.g. fixed vs ARM, credit scores, etc.). We don’t need to dive into too much detail. The G-Fee is relatively constant around 65 bps. There are aspects of it being a political number since higher fees means higher borrowing costs for the average American.

Don’t underestimate the political element at play. Politicians will argue that going public will increase the G-Fee and increase the cost to the average American.

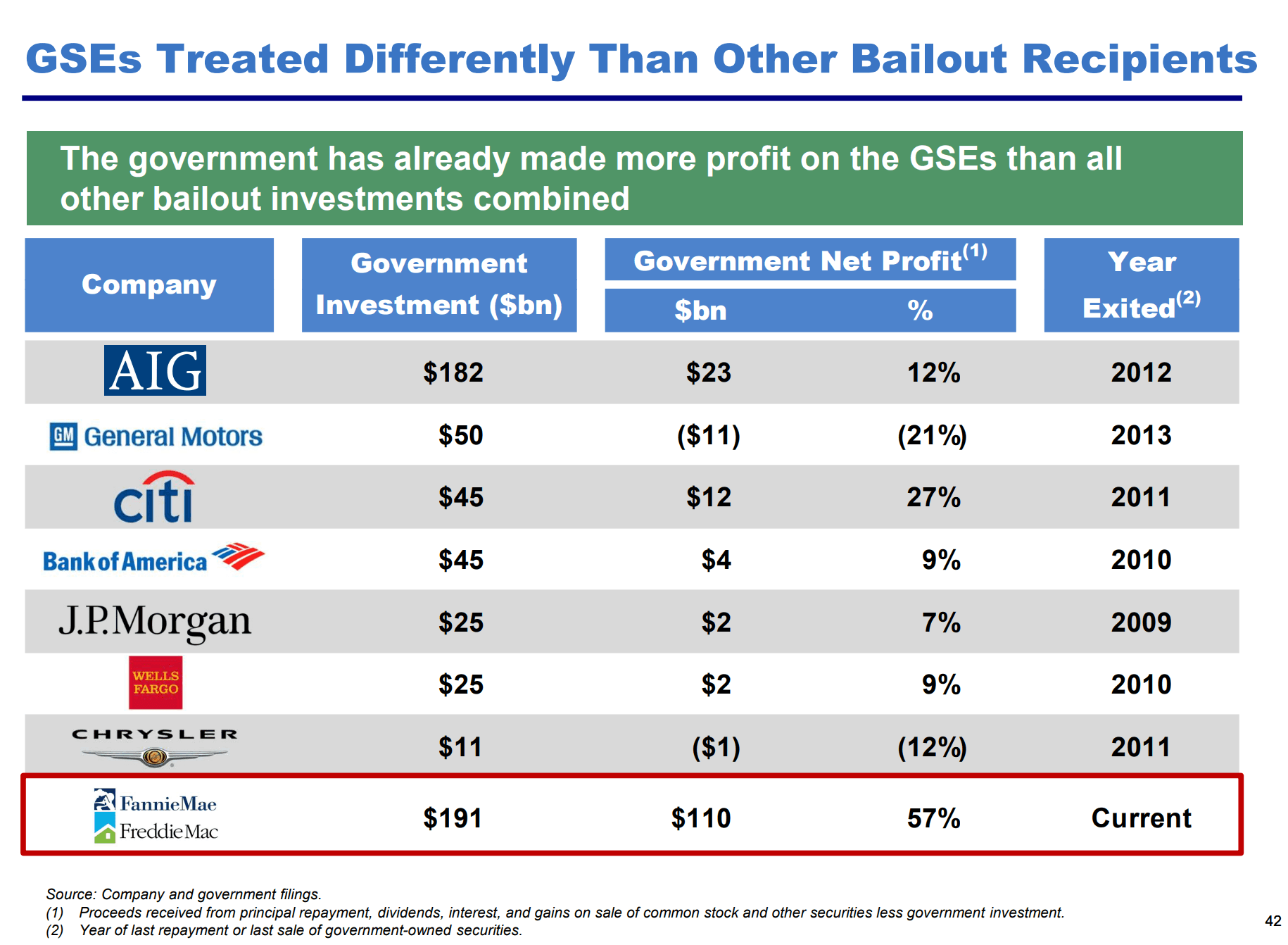

The government has been repaid in full

The Treasury has earned an 11.6% IRR from the 25bn more than what was owed under the original 10% dividend rate (source). Ackman summarizes how other bailouts have performed and it’s clear that Fannie and Freddie are an outlier.

“Competition is for losers”

Thiel would definitely approve of Fannie’s competitive positioning because they’re in a league of their own. As of December 31, 2024 (the latest date for which information is available), Fannie Mae owned or guaranteed an estimated 25% of single-family mortgage debt outstanding and an estimated 21% of multifamily mortgage debt outstanding in the United States (source). Due to the regulations and capital requirements, barriers to entry are enormous.

Financials

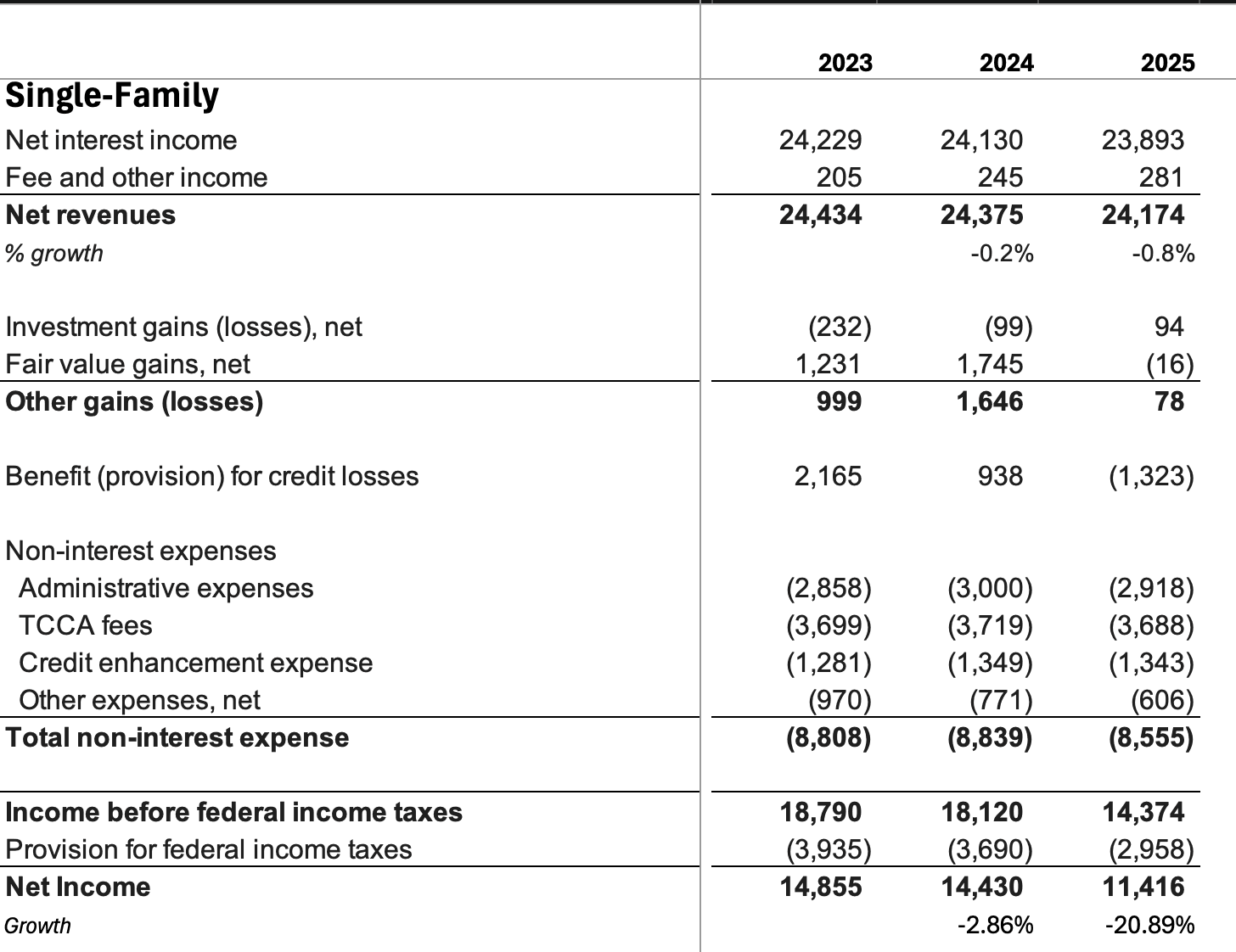

The bottom line is that Fannie is profitable and the credit characteristics on its guaranty book are solid. I’m running a model solely because it feels wrong to not create them, but it’s not a significant driver in the analysis. We can disagree on the US housing market growing at 2% or 0.2%, but unless you’re predicting armageddon then Fannie is on solid footing.

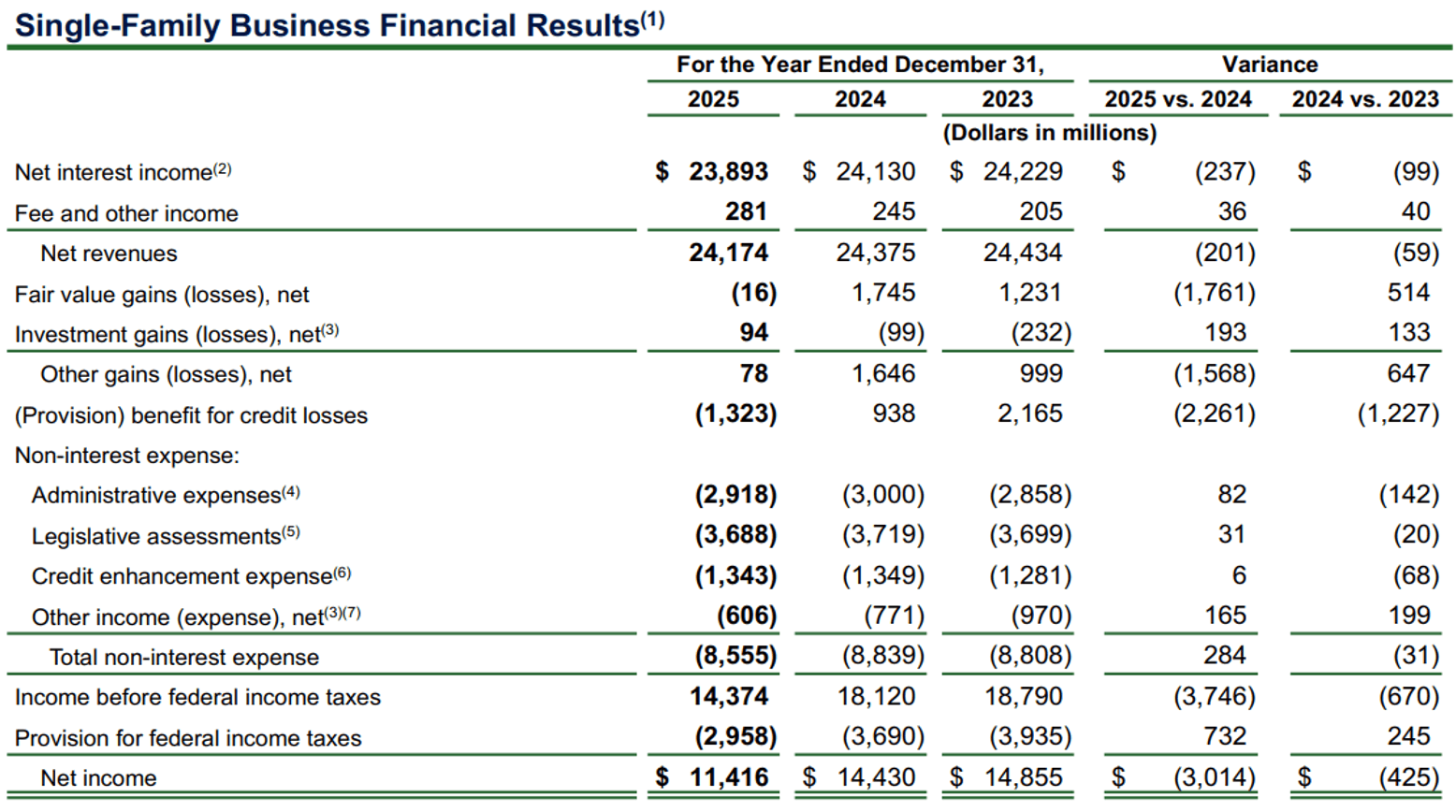

In the interest of brevity, we’re focusing on the single-family segment of the business because that’s ~84% of their net revenue and it illustrates key movements in the business without needing to net out the multifamily segment.

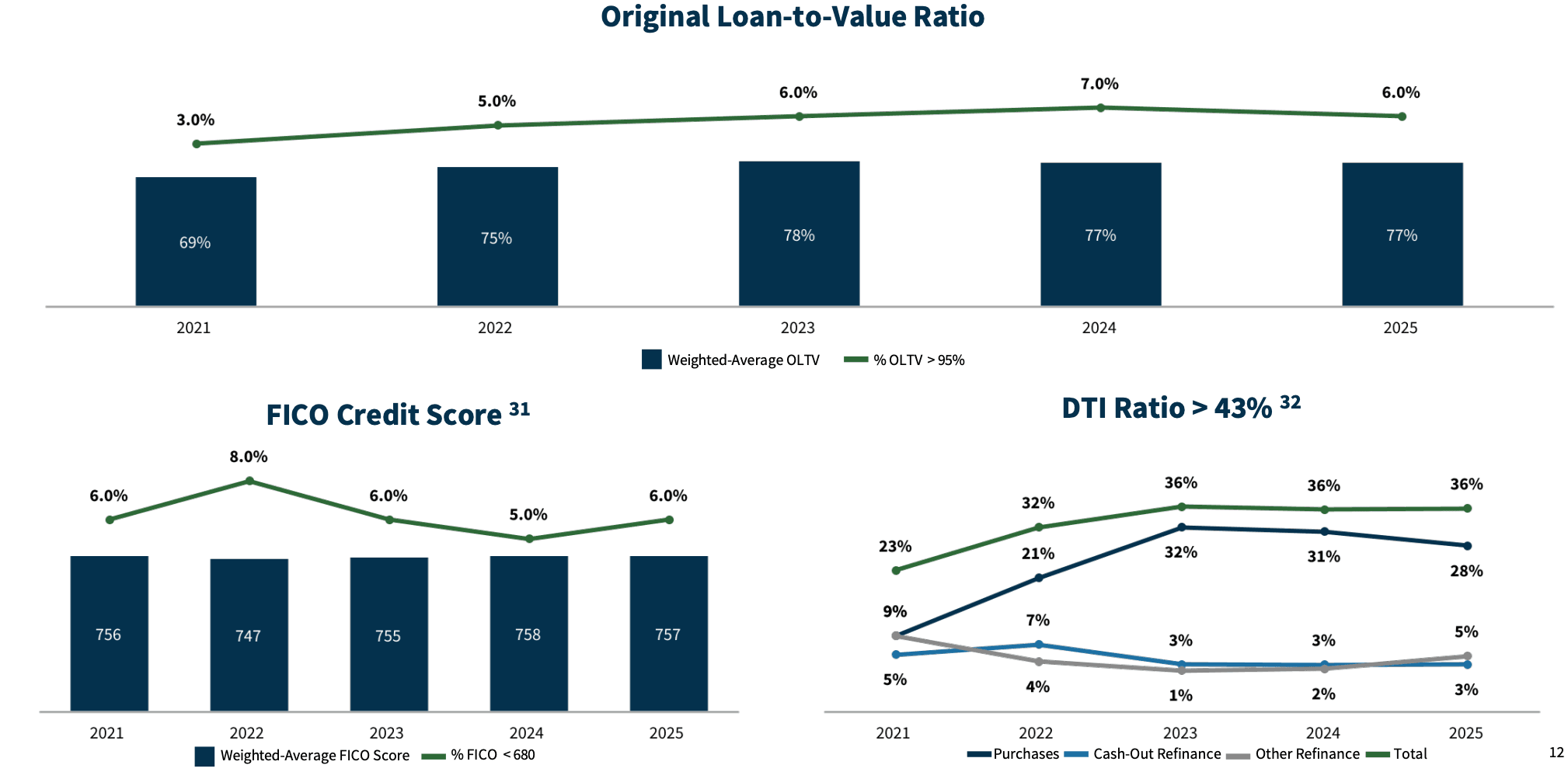

Credit Characteristics

The Q4 ‘25 earnings presentation, summarizes the credit profile. The LTV is under 80%, FICO scores are above 750, and DTI ratios are over 43%.

P&L

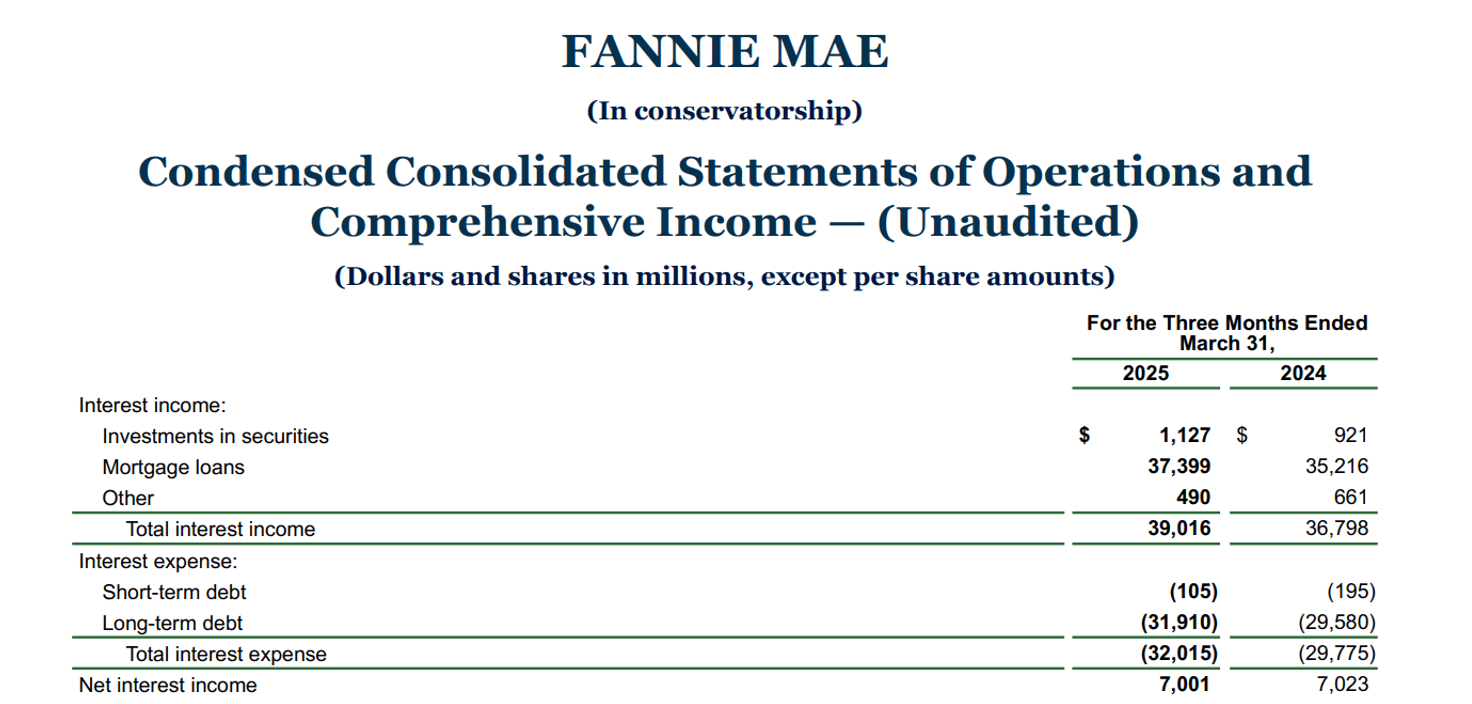

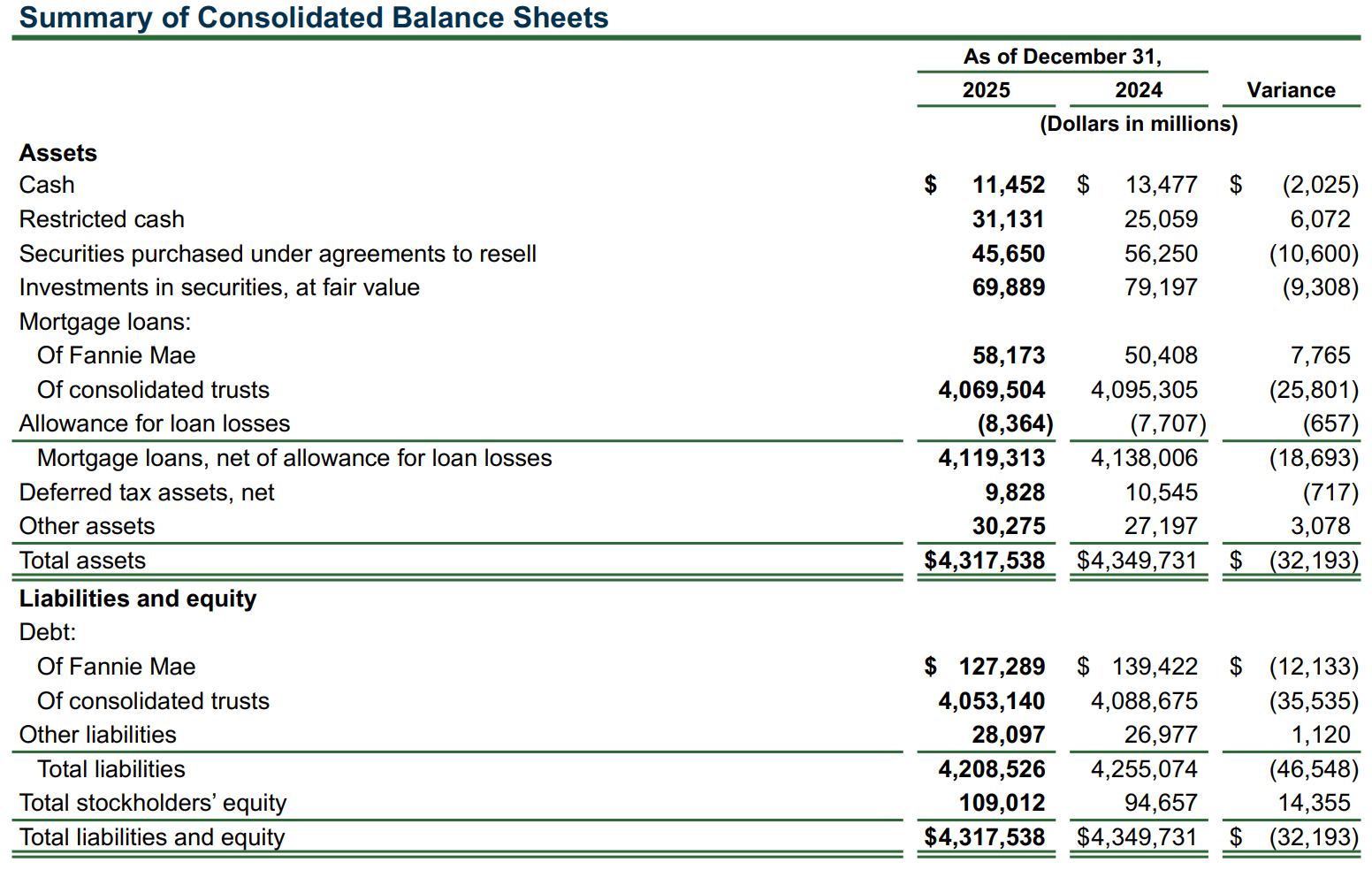

Fannie’s financials can be challenging to read at first glance. When you look at the consolidated income statement, it looks like a spread lender with the “net interest income” line item and $4.1 trillion of liabilities on the balance sheet. Due to the accounting rules, the interest expense and debt both show on the financials, even though the debt and interest payments passthrough to the MBS investors.

The balance sheet shows 4.1 trillion is in consolidated trusts. “Debt of consolidated trusts represents the amount of Fannie Mae MBS issued from consolidated trusts and held by third-party certificateholders.” - 10K.

Net income is solid, despite dropping 20% YoY from 11.4 bln, which is primarily driven by increasing interest rates increasing their provision for credit losses and mark-to-market adjustments for fair value.

Fair value gains/losses on assets flow through Fannie’s income statement, which make earnings appear unnecessarily volatile.

Fannie summarizes it well in the 10K “When interest rates increase, our credit losses from loans with adjustable payment terms may increase as borrower payments increase at their reset dates, which increases the borrower’s risk of default. Rising interest rates may also reduce the opportunity for these borrowers to refinance into a fixed-rate loan. Similarly, many borrowers may have additional debt obligations, such as home equity lines of credit and second liens, that also have adjustable payment terms. If a borrower’s payment on his or her other debt obligations increases due to rising interest rates or a change in amortization, it increases the risk that the borrower may default on a loan we own or guarantee”.

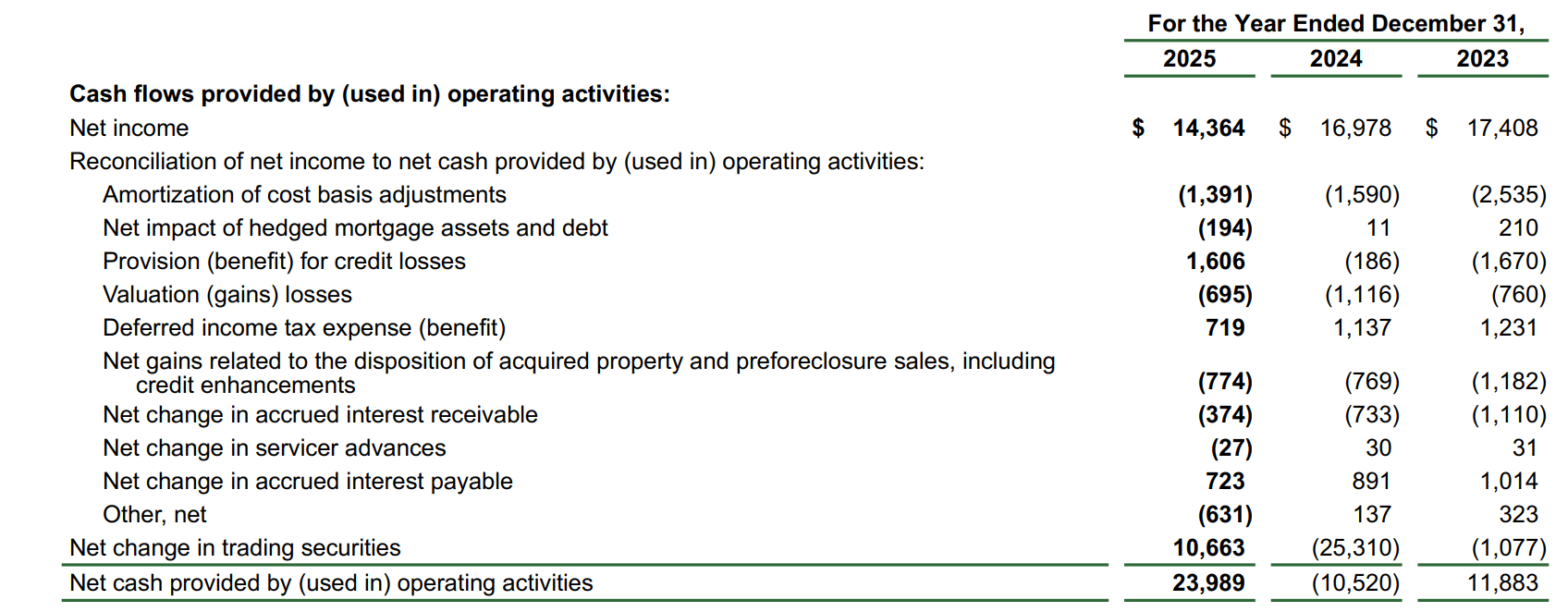

Cash is King

Cash flow from operations is consistently over $10 bln after adjusting trading securities for mark-to-market changes due to interest rates. The decline in cash from operating activities in 2024 was driven by “gains on trading securities in 2024 were primarily driven by holdings of U.S. Treasury securities moving closer to maturity. As a result, previously recognized fair value losses were reversed, resulting in a net gain on our fixed-rate securities held in our corporate liquidity portfolio.”

Risks

1. Status-quo: nothing happens and conservatorship persists

Risk

Never underestimate the government’s ability to muck up the waters. Given Fannie has been in conservatorship for 18 years, there’s not much of a reason why they can’t be in conservatorship for several more years.

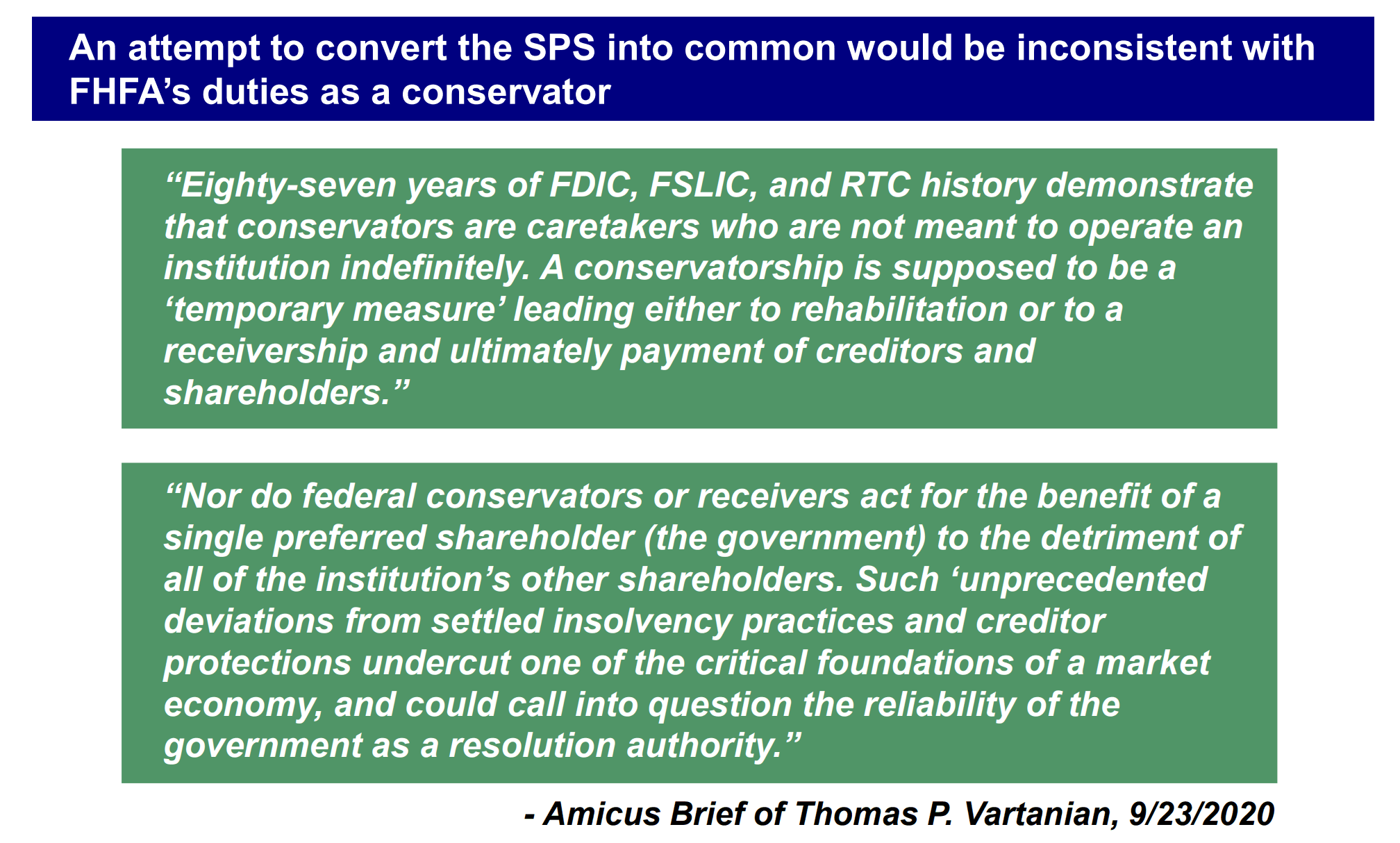

Ackman’s presentation references an amicus brief with the Supreme Court, and to the casual reader, this appears to provide overwhelming support for a long position in the stock.

Context is important though. That brief was filed in September 2020. Its purpose was to prevent the FHFA from sweeping 100% of earnings to the Treasury. As you know, the amendment to sweep earnings was created. While those quotes may seem convincing to you and me, they weren’t convincing to the Supreme Court.

In June 2021, Collins vs Yellen, the Supreme Court agreed with the FHFA and stated “The Recovery Act grants the FHFA expansive authority in its role as a conservator and permits the Agency to act in what it determines is “in the best interests of the regulated entity or the Agency.”

Mitigation

This mitigation is admittedly handwavey. Conservatorships are meant to be temporary. The SPS shares have been repaid. Fannie is profitable and its portfolio has strong credit characteristics. There’s not much incentive, economically or legally, for the government to keep Fannie in a conservatorship.

2. Senior Preferred Stock Conversion into Common Stock

Risk

This is a thorny issue. On the surface, the government has no right to convert their preferred shares into common. The fourth amendment makes this very clear, *“The holders of shares of the Senior Preferred Stock shall not have any right to convert such shares into or exchange such shares for any other class or series of stock or obligations of the Company”.*However, the government has full control over Fannie and can update amendments as they deem fit. Remember that amendment to sweep 100% of earnings?

Mitigation

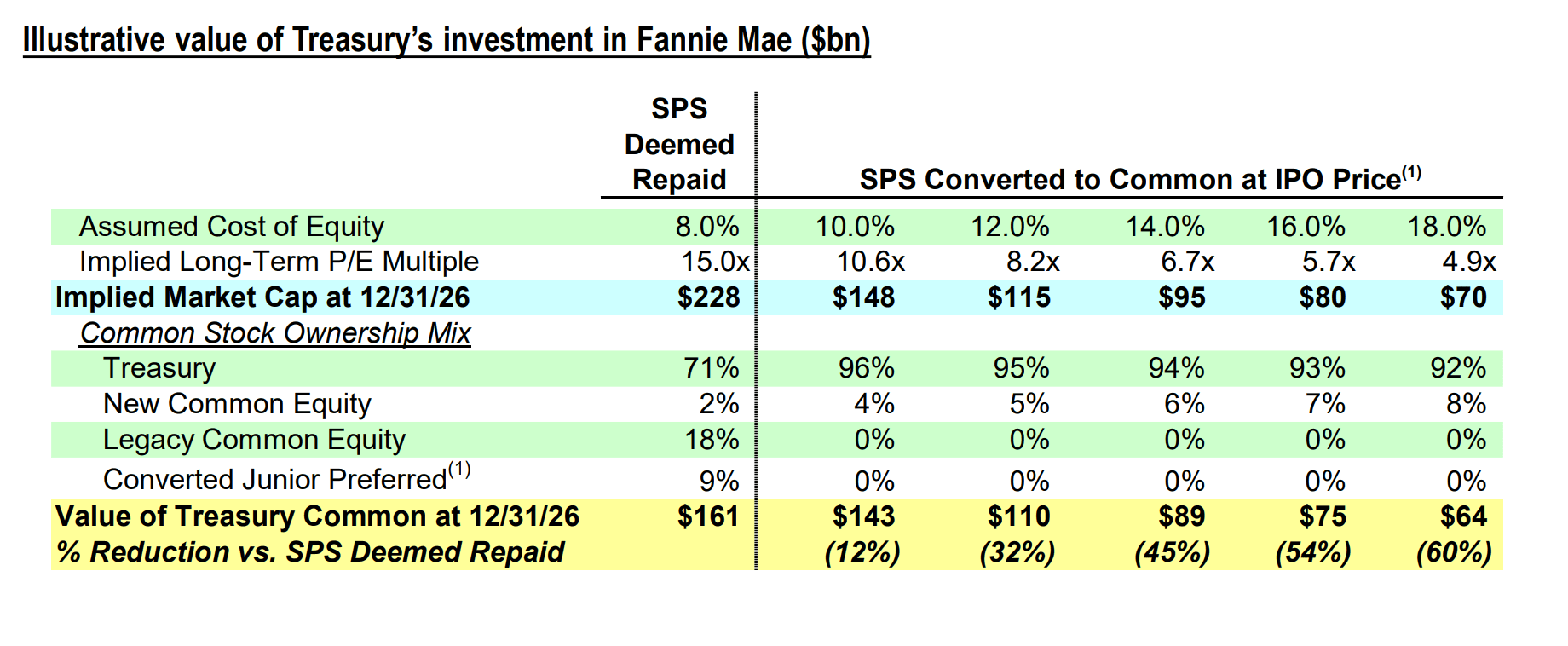

This is the reverse of moral hazard with government bailouts. The government already owns 80% of Fannie via the warrants. Converting the SPS shares to common would lower the valuation multiple. Who wants to invest in a company that is 95% owned by the government and the government has set a precedent for not acting in the best interest of all shareholders? The government will earn more money by not converting the SPS shares into common and effectively owning 80% of a more valuable company than 95% of a less valuable company.

Ackman provides illustrative financials below. If the SPS is deemed repaid and the PE multiple is 15x then the implied market cap is 148 bln if the Treasury converts SPS into common and the market assigns a 10.6x multiple.

3. Capital Requirements

Risk

What should be the capital requirements post-conservatorship?

This gets into the weeds of regulatory requirements. While Fannie is in conservatorship, it does not have to comply with the capital requirements. We’re going to reconcile the regulations with the tables Fannie reports so it’s clear how the numbers are being calculated.

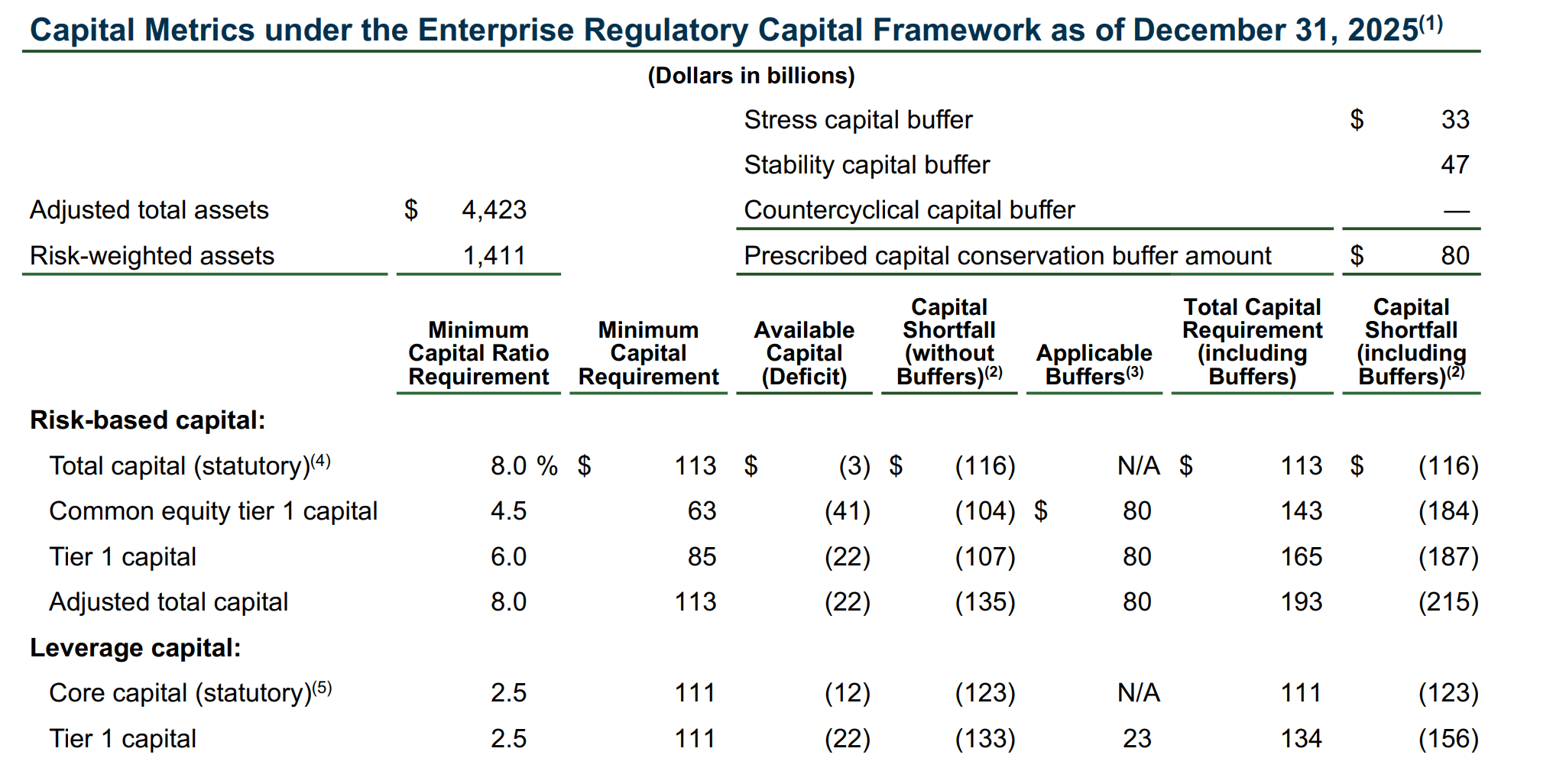

Current state**: adjusted total capital** must be 8% of risk-weighted assets, tier 1 capital is 6% of risk-weighted assets, etc.

Future state**: compliance** is not required until the conservatorship ends. There’s a leverage buffer requirement of 4% the adjusted total assets.

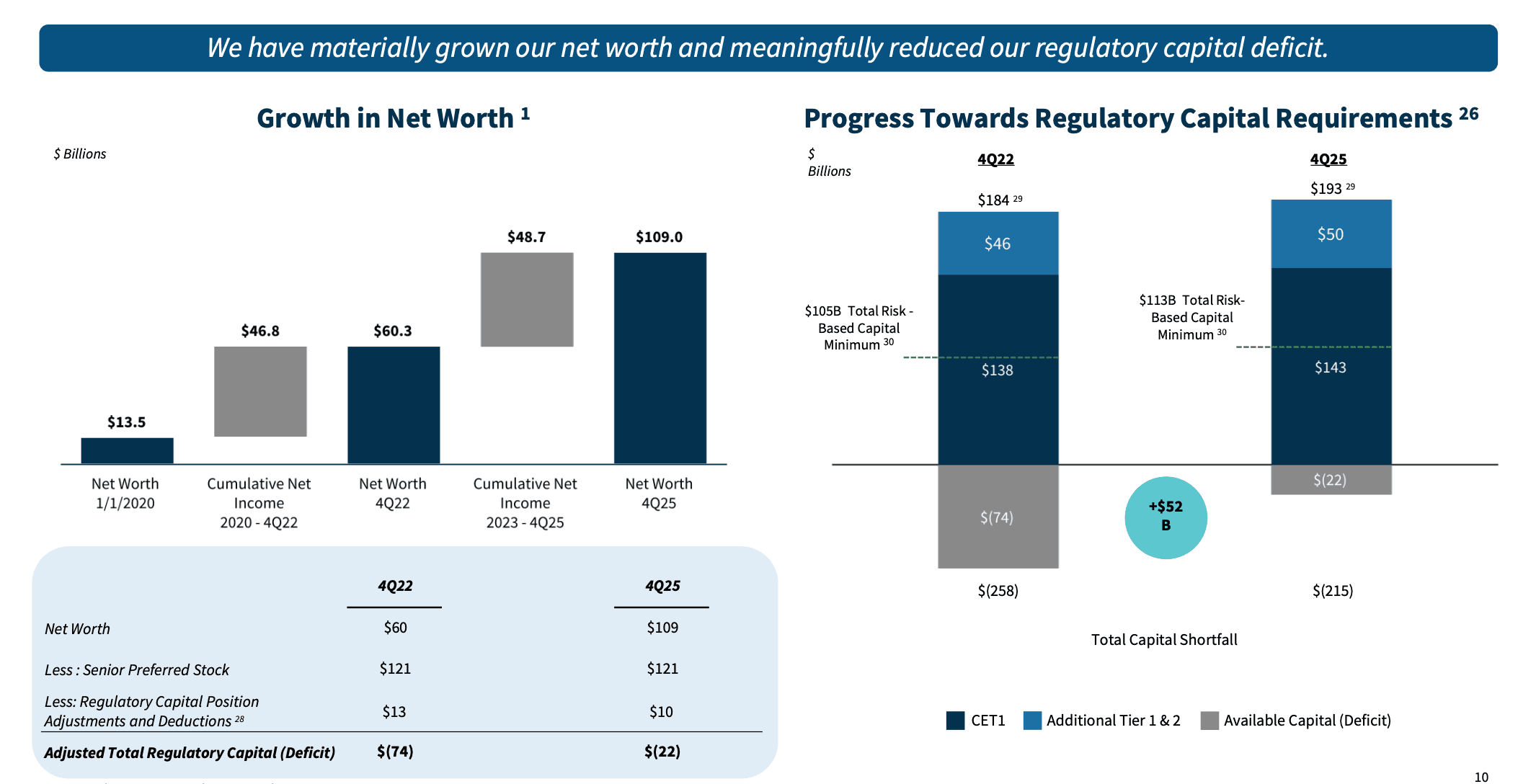

Reporting: earnings presentation vs 10K

Fannie’s earning presentation glosses over key parts of this issue. When you read their slides, progress has been made towards regulatory capital requirements, they’ve increased their capital by 22 bln. That’s true - they even circle it in a nice big turquoise bubble. But, notice that small $(215) bln number floating in the bottom right corner of the chart. Let’s dig into that.

Management clearly states in the in the most recent 10K, “We are significantly undercapitalized and may be unable to fully satisfy our regulatory capital requirements. As of December 31, 2025, we had a 215 billion shortfall to our risk-based adjusted total capital requirement including buffers.

It’s easy to conflate these numbers; let’s establish key metrics: i) minimum capital requirement, ii) available capital, and iii) capital requirements including buffers.

Total risk-weighted assets are 113 bln. They have available capital of negative 135 bln capital shortfall.

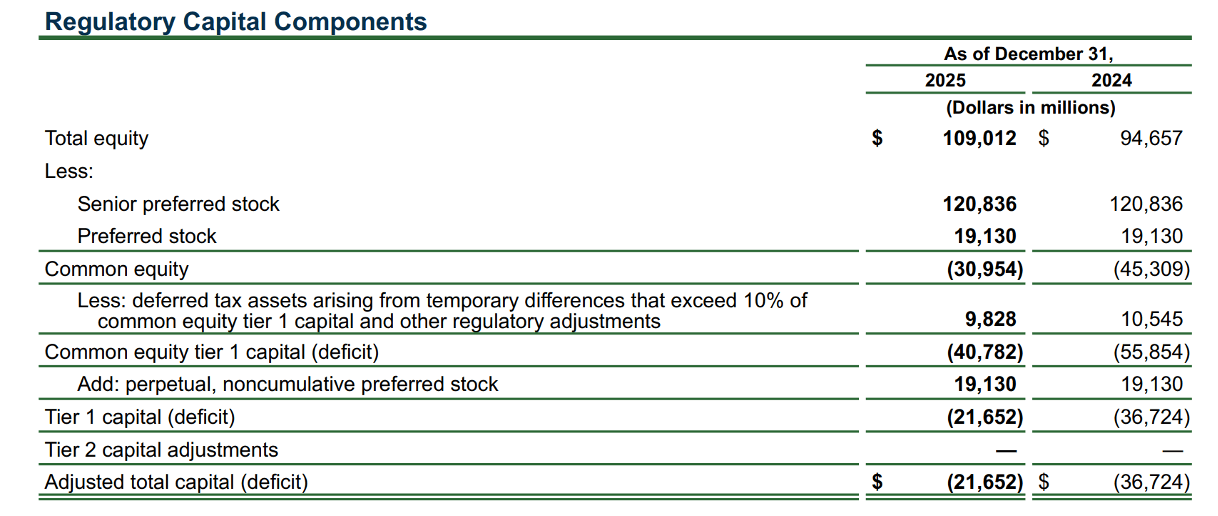

The negative $22 bln of available capital is driven by the preferred stock that is netted out of the equity.

All of this reporting only covers the current state.

Transition period

There’s still the 4% leverage requirement once the conservatorship ends. “The enterprise regulatory capital framework has a transition period for compliance. We are currently subject to the requirements to publish quarterly capital reports, submit capital plans to FHFA, and provide prior notice to, and obtain approval from, FHFA for certain capital actions; however, we are not required to comply with the minimum capital requirements or the buffer requirements while in conservatorship. The compliance date for the minimum capital requirements will be the date of termination of our conservatorship or such later date as FHFA may order.” - 10K.

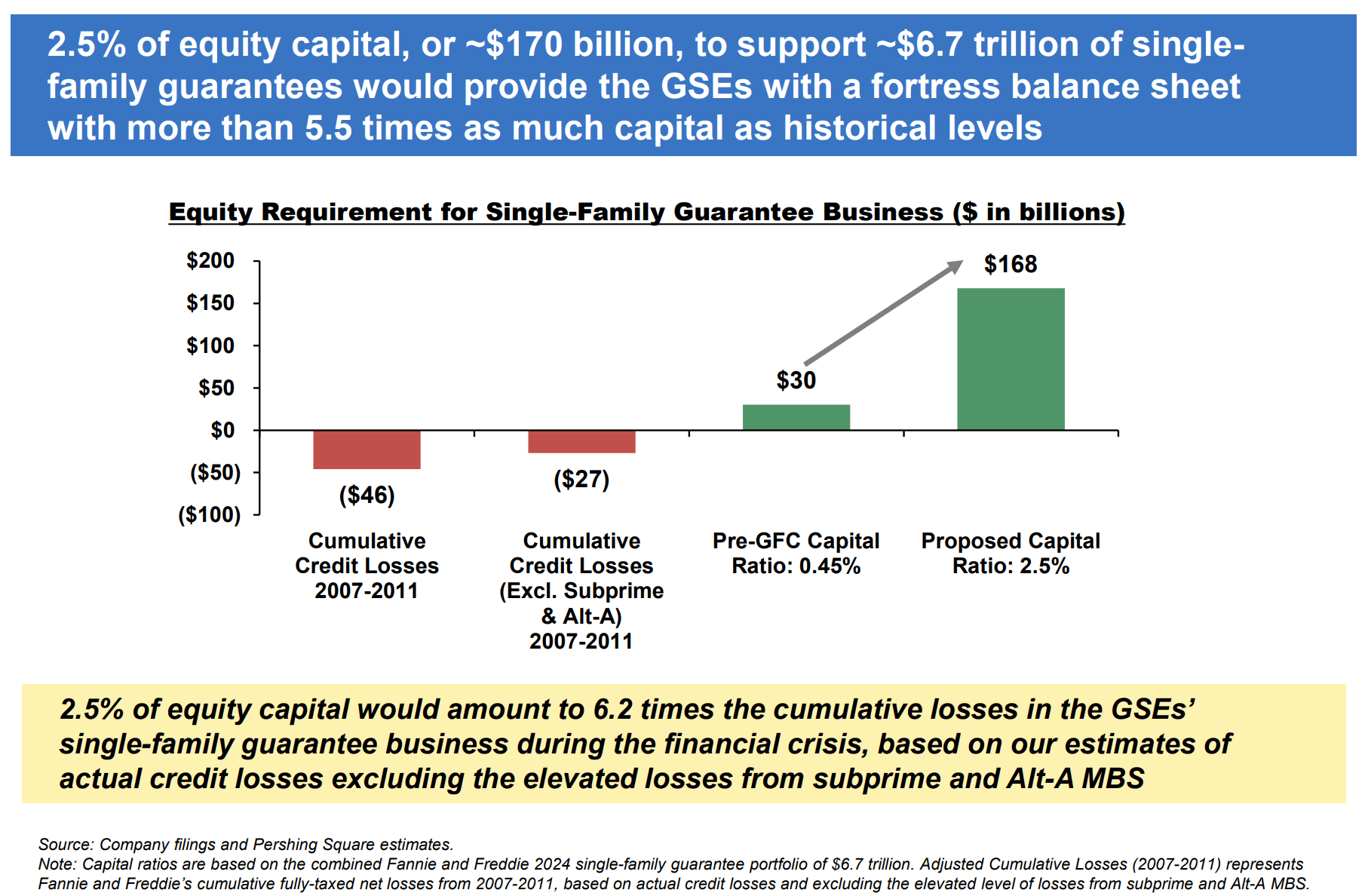

A decrease in the leverage ratio from 4.0% to 2.5% would result in 4.4 trillion) of less capital required.

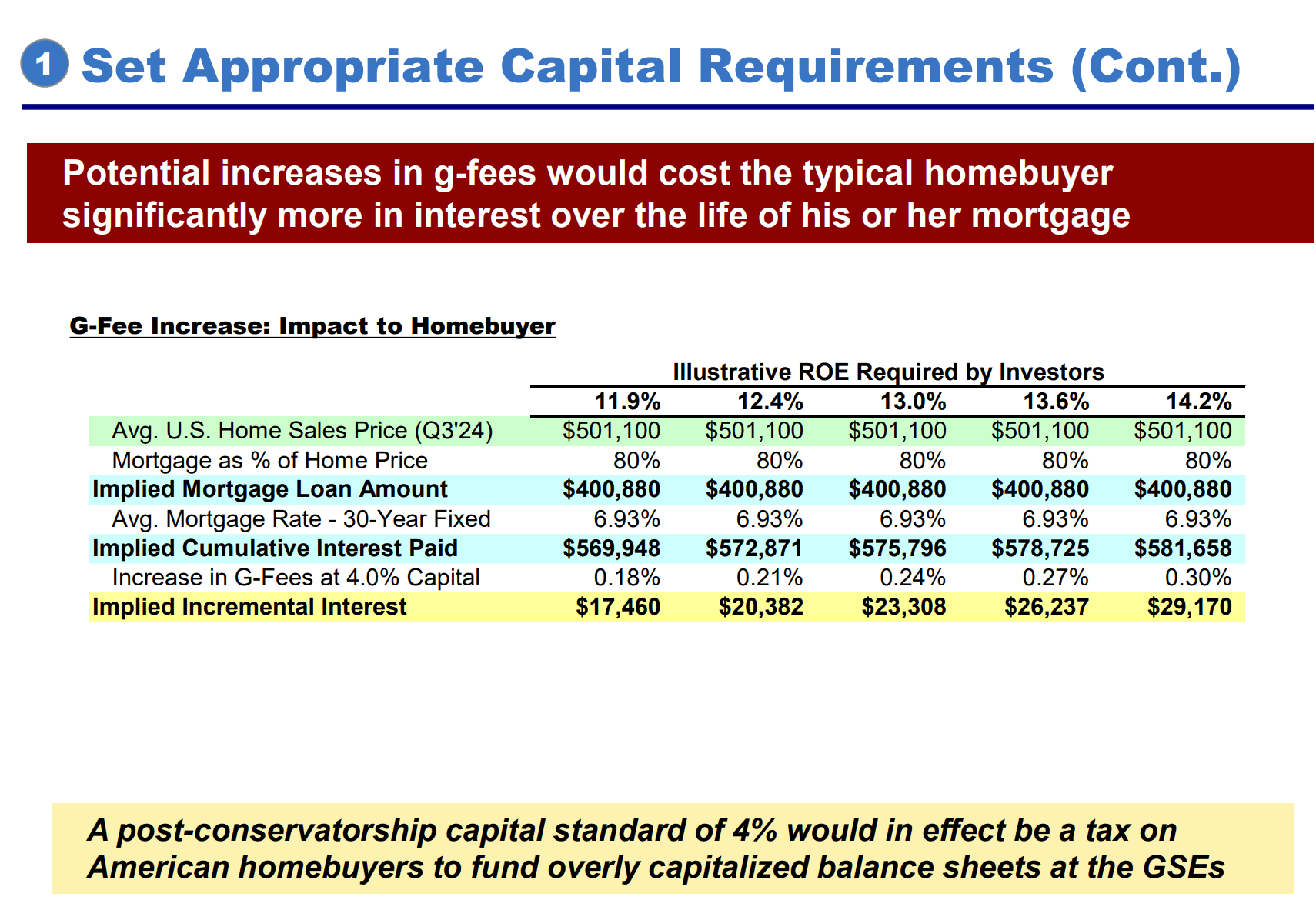

Ackman has a slide showing how an increase in capital requirements for Fannie Mae is effectively a tax on American homebuyers.

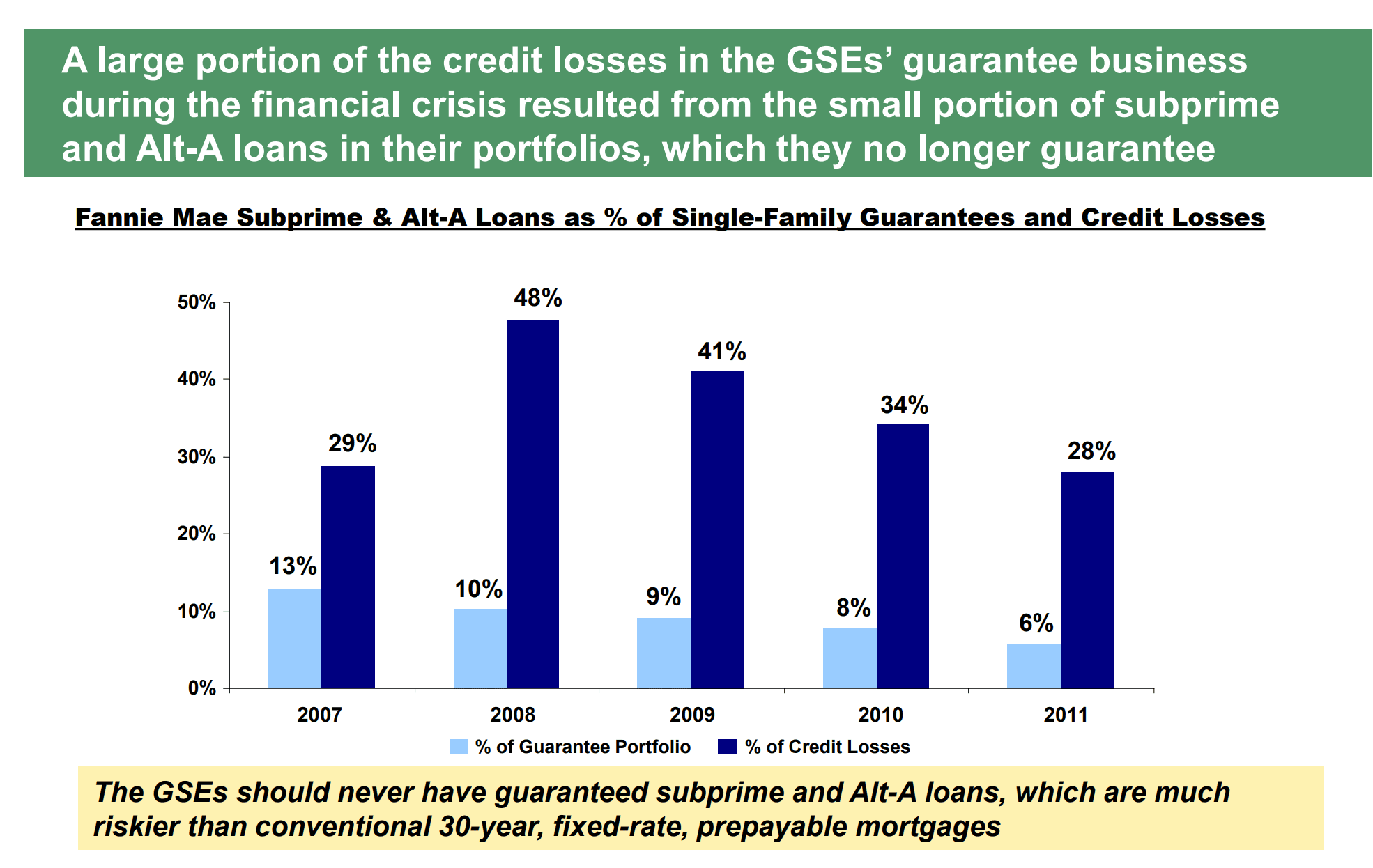

How do we know if 2.5% or 4.0% is a reasonable capital requirement?

Ackman has a nice slide showing that cumulative credit losses for Fannie and Freddie were 27 bln if we exclude subprime loans (which Fannie doesn’t offer anymore).

In fairness, there might be accounting magic in his calculations. Fannie’s 2011 10K, shows 46 bln for 2007 - 2011 for Fannie & Freddie combined. His slide footnotes that “[losses] represents Fannie and Freddie’s cumulative fully-taxed net losses from 2007-2011, based on actual credit losses and excluding the elevated level of losses from subprime and Alt-A MBS”.

Taking a tax-advantage on the losses certainly seems aggressive from a risk management perspective - you can’t use future tax losses to pay today’s creditors. But, I’m going to stop picking apart this slide because: a) it’s a terrible networking tactic and b) the larger point still stands: a leverage ratio of 2.5% is sufficient.

How to meet the capital requirement

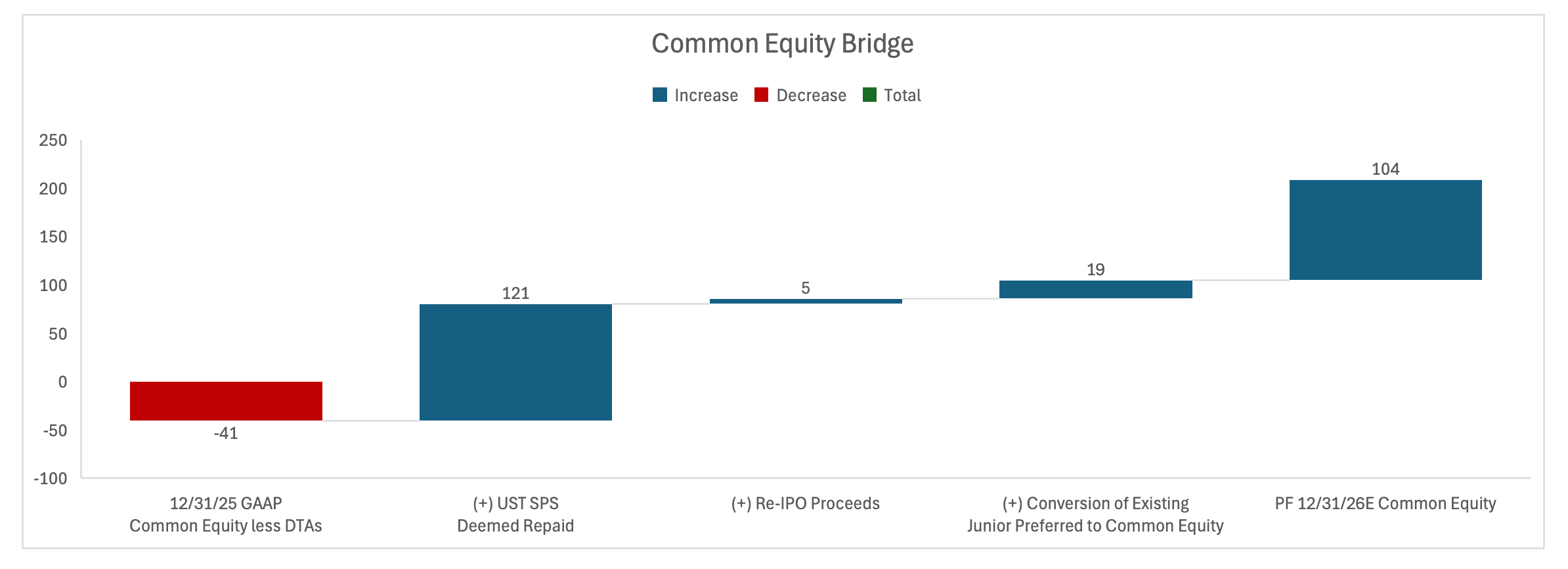

Capital required would be 4.4 trillion. Under those capital rules, Fannie will have sufficient capital to IPO this year.

The equity bridge below assumes the SPS is deemed repaid, junior preferred is converted to common, and a 104 bln of capital. Fannie has net income around 7 bln capital shortfall this year.

Mitigation

We’re relying on regulators to set reasonable capital requirements. If this becomes a highly politicized topic, then we can ignore the economics and the incumbent political party will set the requirement as they see fit. If cooler heads prevail, then 2.5% should be reasonable.

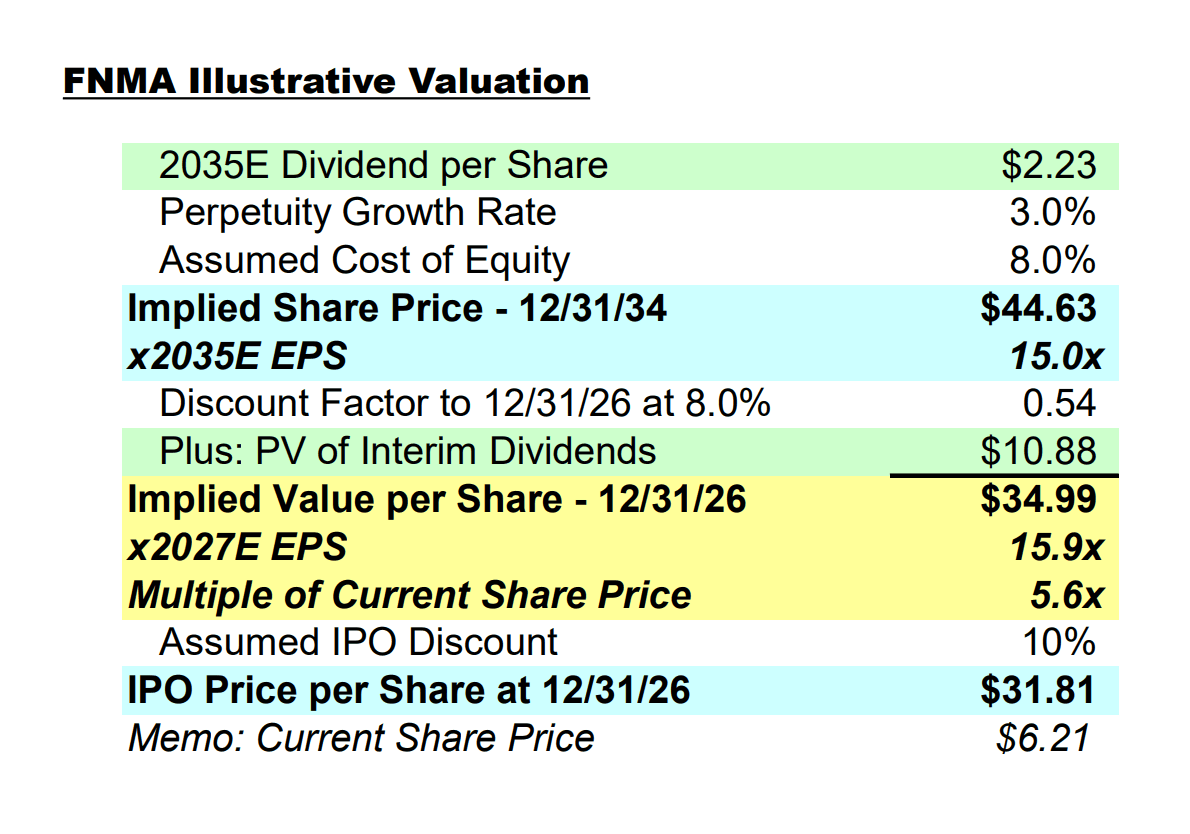

IPO

Ackman calculates an IPO price of 2.23.

These financials might be optimistic - even Ackman’s presentation calls the model “illustrative”. Net income has declined 15.4% and 2.5% in 2025 and 2024, respectively. Nonetheless, that’s not a cash number (see our financial analysis section), and he’s only showing a 3% CAGR for net income from 2025 - 2035. Reasonable people can disagree on the validity of the model with +/- 15% but I wouldn’t expect it to deviate far from that.

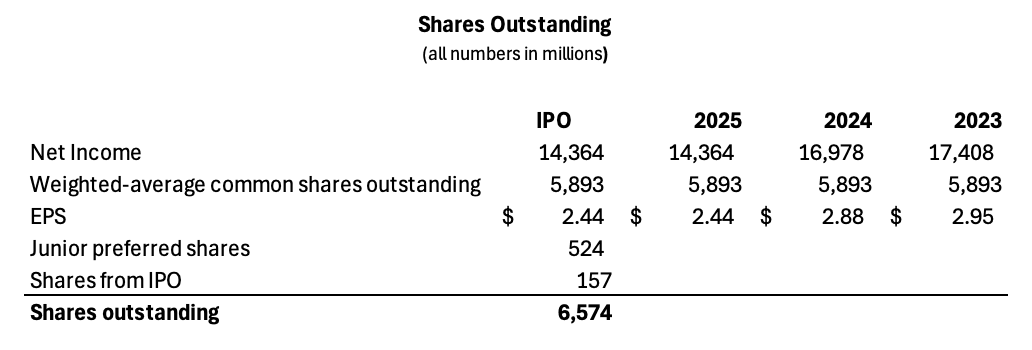

IPO mechanics: we’re showing a 12% increase in shares outstanding in the model because we’re converting junior preferred to common and issuing 157 million shares in the IPO.

Opposing Views

- “Economists have warned that reprivatizing the Enterprises could have disastrous effects on the mortgage market, driving up costs for homebuyers even further. For example, some experts have estimated that mortgage rates could increase by up to 1% in the first year of privatization alone.”

NPR: Privatizing Fannie Mae is risky. Would it be a win for taxpayers or Trump’s donors?

- “The idea, promoted by Federal Housing Finance Agency (FHFA) Director Bill Pulte and Trump himself, has alarmed critics, who warn that unwinding the 17-year federal conservatorship of the two firms could rattle financial markets and drive up mortgage rates, while potentially generating billions of dollars for key Trump supporters. Pulte has said the administration is "looking to extract … value from [Fannie and Freddie] for the benefit of the U.S. taxpayers."“

- " I am very worried that the Trump administration is very focused on how the billionaires are gonna do in any Fannie/Freddie deal," Warren told NPR, "and not paying any attention at all to what the young family that's hoping to buy their first home is gonna do as a consequence of any deal."

- Yin, a professor of public policy at UCLA Luskin with a joint appointment at the UCLA Anderson School of Management, warns that the current approach lacks transparency and could dismantle critical safeguards established after the 2008 financial crisis. “A hasty insider-driven IPO and exit from conservatorship will erode the safeguards that have kept the housing market stable, exacerbate systemic risks, and primarily enrich shareholders,” he says. “Such a move would align with the Administration’s agenda of rolling back other financial regulations and oversight.”

Supporting Views

- Fannie and Freddie now back more than 60% of new mortgages, compared with roughly 45% before the 2008 financial crisis. the government takeover of mortgage finance severely limits innovation. Mortgage originators will make only loans that conform to Fannie and Freddie’s rules. The 30-year fixed-rate mortgage is a prime example. This product, designed in the 1940s, is unsuited to many of today’s homeowners. If you take out a 3% mortgage and rates rise to 7%, you can’t take the 3% with you if you move. Other countries allow homeowners to take that protection with them.

- Fannie Mae and Freddie Mac: How Government Housing Policy Failed Homeowners and Taxpayers and Led to the Financial Crisis

Next Steps

- The class action lawsuit is under appellate review with oral arguments scheduled for Tuesday, April 21, 2026 at 9:30am

- Wait for guidance from the Bill Pulte (Federal Housing Director) or from Trump. “President Trump keeps options on the table — all options at all times,” Pulte said on Fox Business when host Maria Bartiromo asked him about the potential for public offerings of the government-sponsored mortgage giants. “But the reality is, we don’t have to do that.” - Politico

For informational purposes only — not investment advice.