CPI down, equities up.

TLDR

Good macro data beat bad geopolitical headlines.

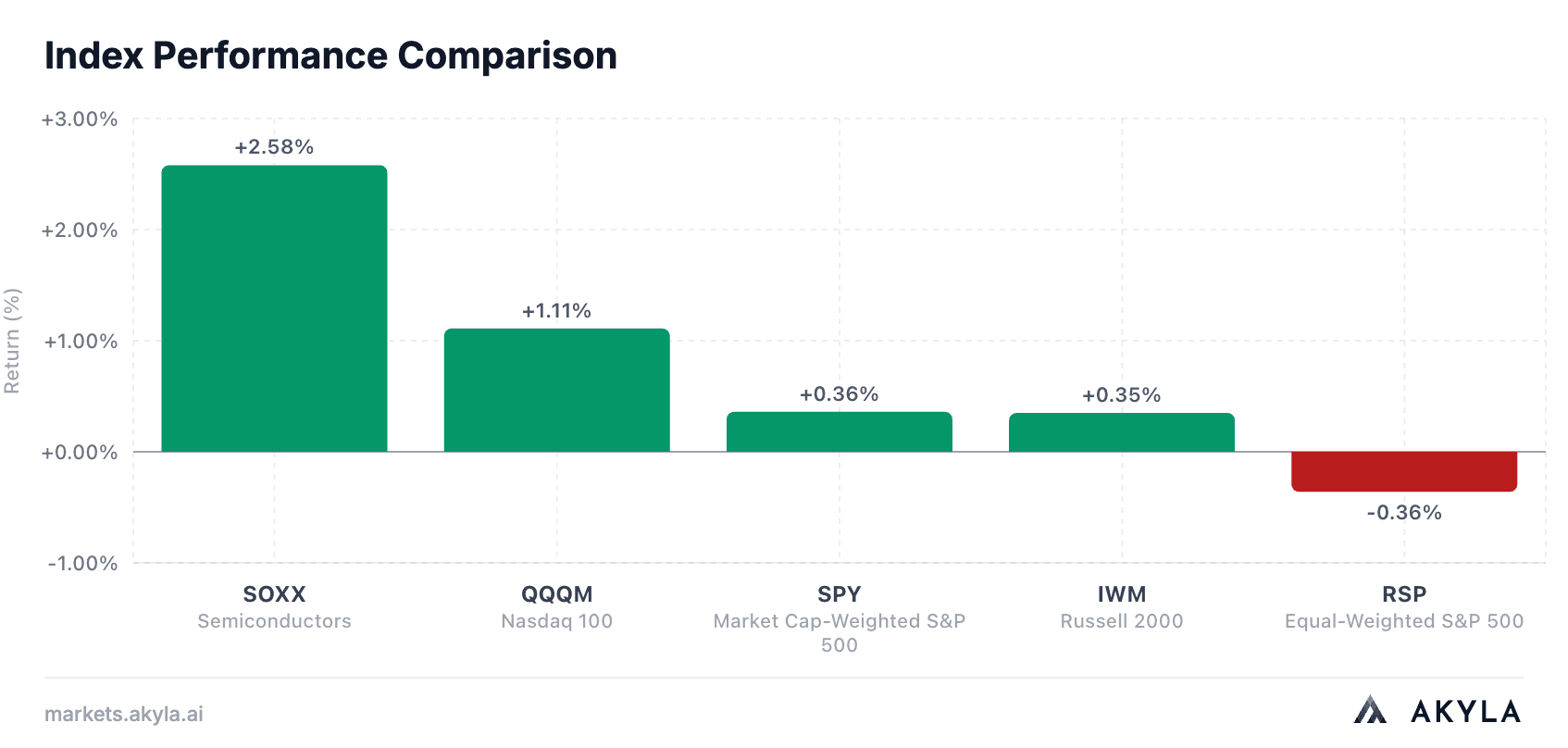

Equities bounced after a softer-than-expected CPI report. The S&P 500 rose 0.36% and Nasdaq gained 1.11%. The cleanest read is that investors were willing to buy growth again because inflation cooled, Treasury yields fell, and the market reduced the probability of a near-term Fed hike.

But this was not a perfect tape. Oil kept rising because the U.S.-Iran conflict is still active, high-yield spreads widened slightly, and equal-weighted equities lagged. The market is not panicking, but the risk is obvious: June CPI looked good because energy prices fell, while July oil is already moving the other way.

The market is saying: inflation improved, but the inflation risk did not disappear.

Equities

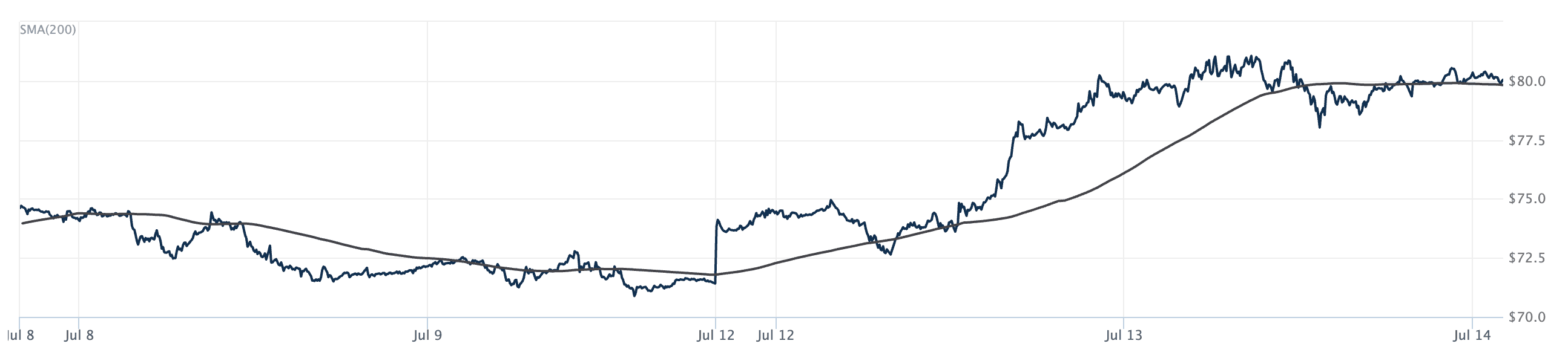

Tech and large caps mostly bounced back from Monday's terrible day. SOXX was up 2.5% compared to Monday's close. Likewise, the Nasdaq and SPY we're both up as well 1.11% and 0.36%, respectively. The equal-weighted S&P 500 was down though, signaling that markets are still on weak footing.

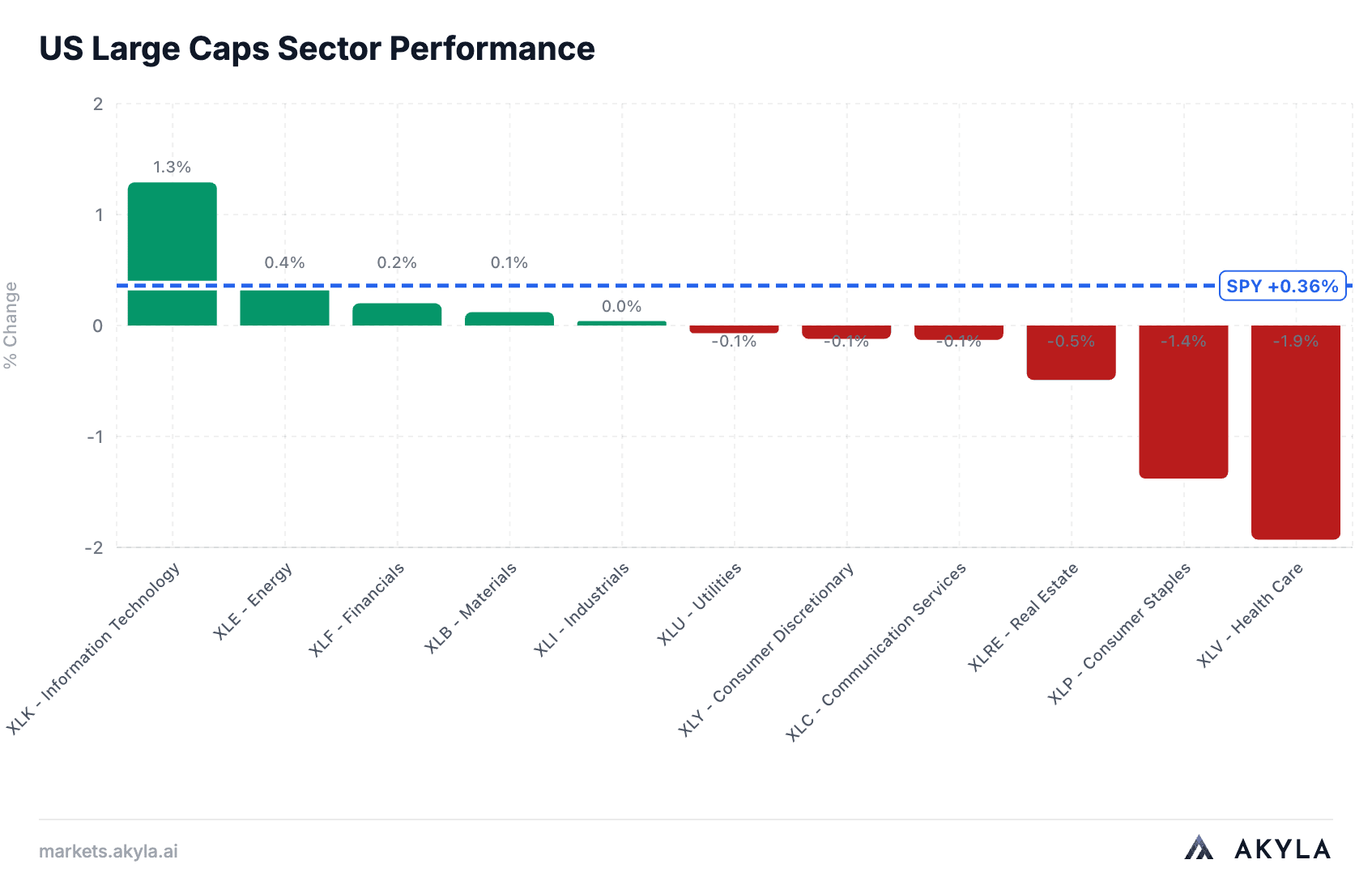

We can see technology, energy, and financials were all up. Financials we're driven by huge profits reported at the bulge bracket banks.

Options

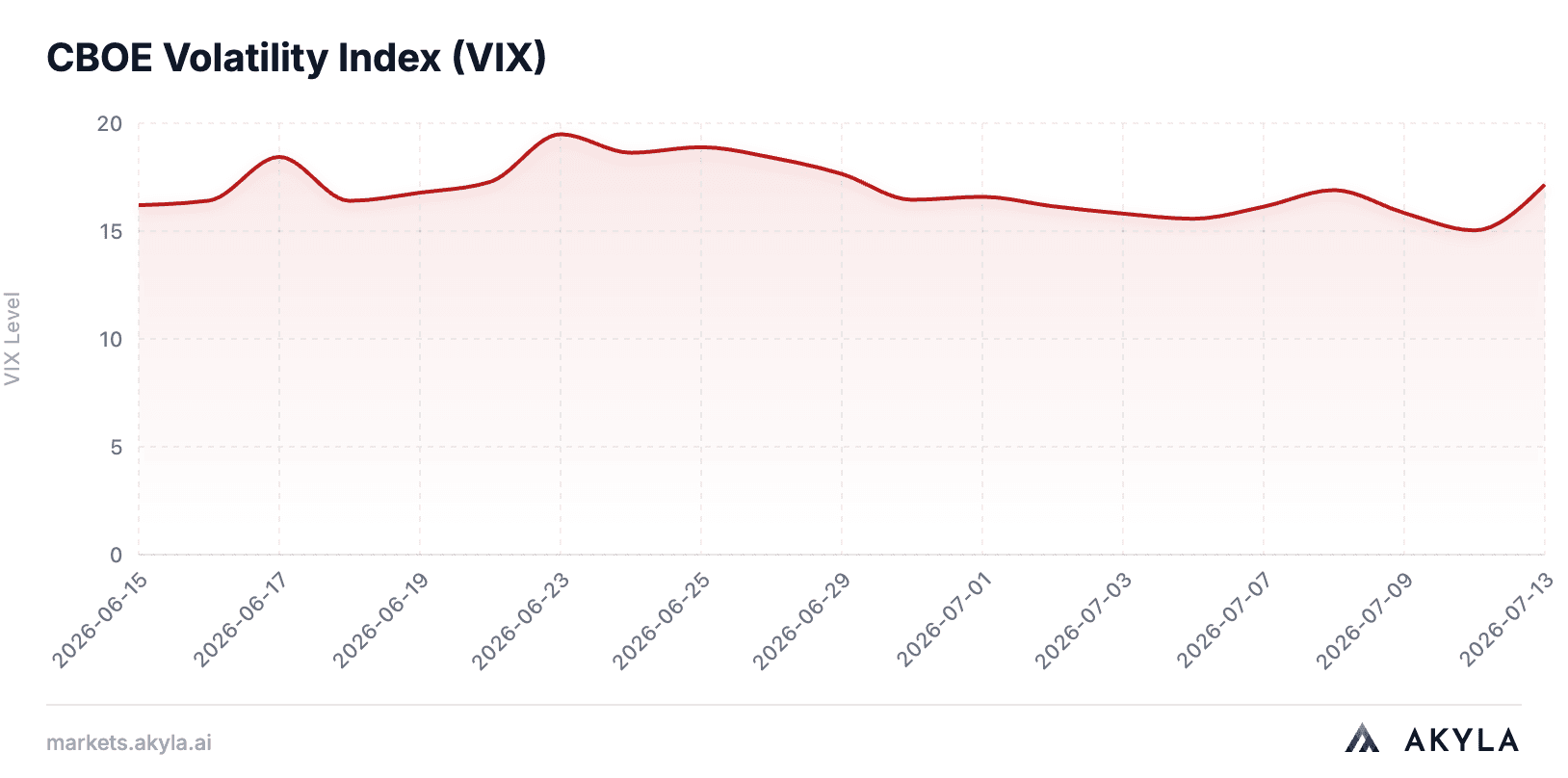

VIX is climbing higher to ~17 but it hasn't been particularly insightful lately. We'd look for it to break out to significantly lower/higher levels to derive meaningful takeaways.

Rates & Spreads

Commodities

WTI is increasing as the Iran war continues.

Macro

The macro headline was CPI.

Headline CPI fell 0.4% month-over-month in June after rising 0.5% in May. On a year-over-year basis, inflation slowed to 3.5% from 4.2%. Core CPI also improved, rising 2.6% year-over-year after 2.9% in May.

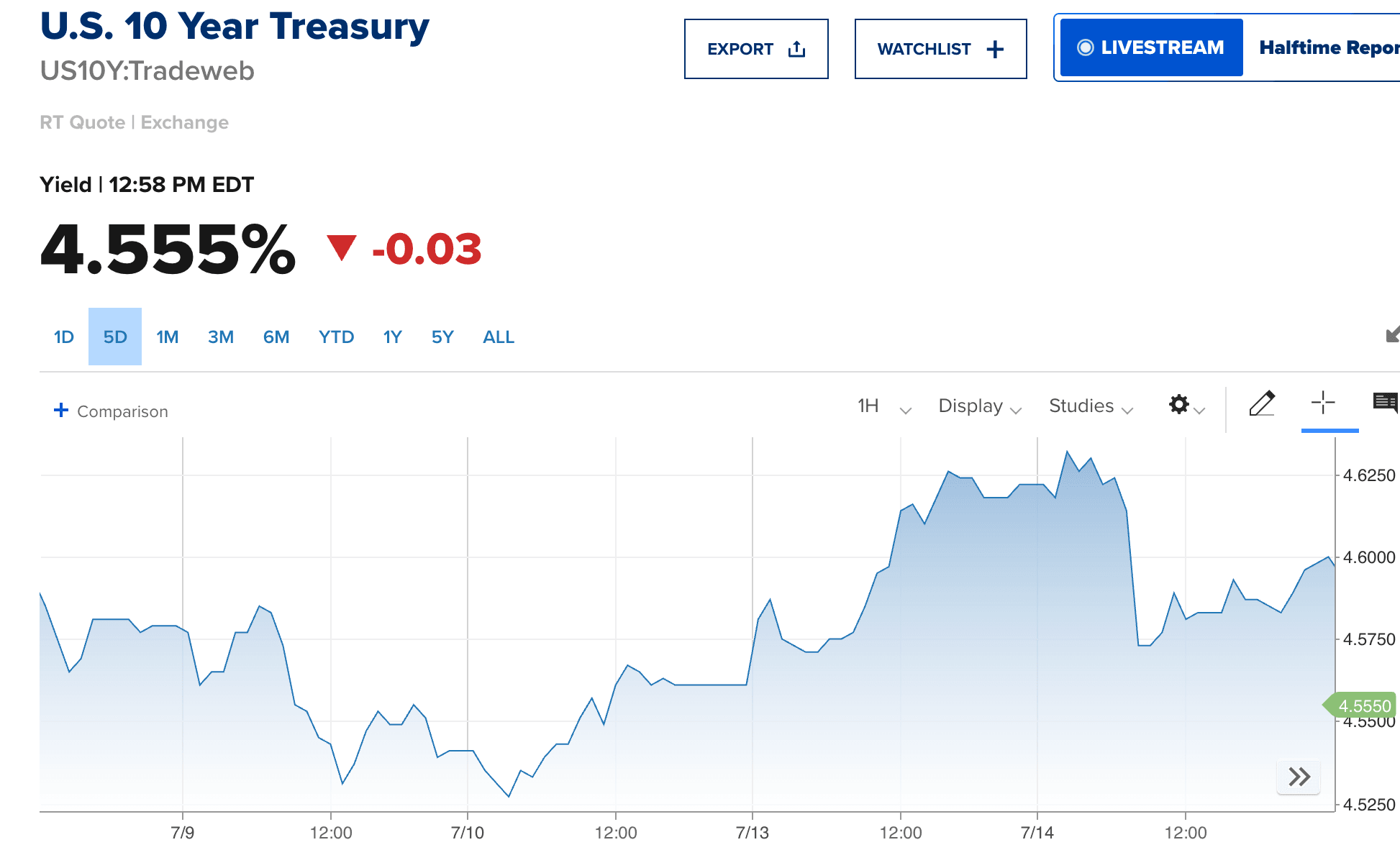

That is a legitimately good report. It reduced pressure on the Fed to hike immediately and helped Treasury yields fall. The 10-year Treasury yield declined to 4.589%, while the 2-year fell to 4.196%.

Fed officials were constructive but not dovish. Chair Warsh and Chicago Fed President Goolsbee both treated the CPI print as encouraging but emphasized that one soft report is not enough. Markets reduced the probability of a July hike to around 15%, but September still looks live. That is the setup: inflation data finally gave the market relief, but the Fed is not declaring victory.

For informational purposes only — not investment advice.