The market looks healthy. Timid but healthy.

TLDR

Market stress indicators still look healthy, but the tape was quieter than Thursday.

VIX fell to 15.03, oil moved lower, and high-yield credit spreads remain tight. That is still a constructive backdrop. The market is not acting like it sees systemic stress.

Equities

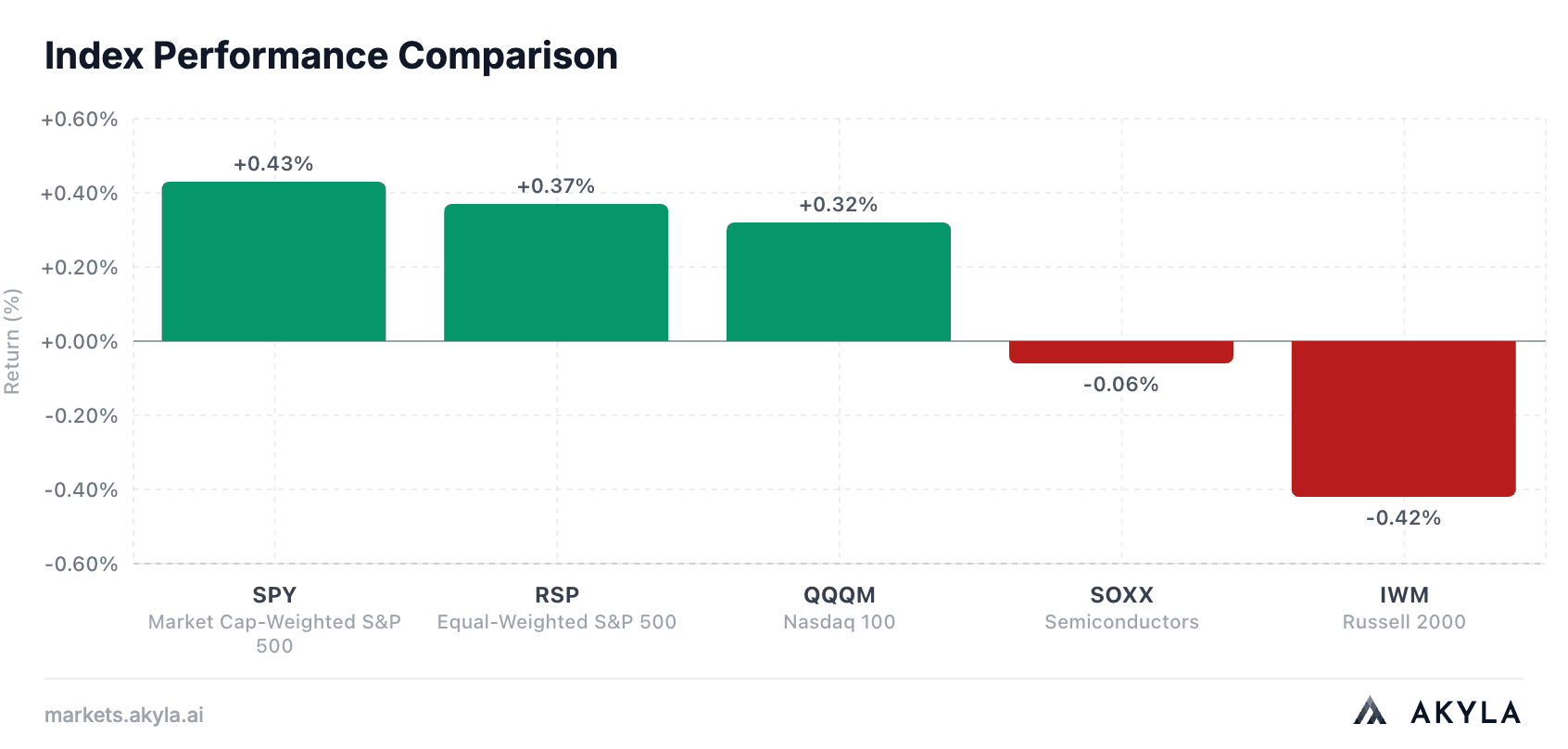

Equities were positive, but the move was not especially exciting.

Equities finished modestly higher. SPY was up 0.39%, QQQM was up 0.31%, and RSP was up 0.37%. The S&P 500 rose 0.4%, the Nasdaq rose 0.3%, and the Dow rose 0.3%, while small caps lagged, with the Russell 2000 down 0.5%.

Small caps were weaker, with the Russell 2000 down 0.5%. That is the one equity-market negative worth flagging. If the market is truly broadening, small caps should participate. Today they did not.

Semis were mixed. SMH was up 0.60%, while SOXX was slightly down. That tells me the AI bid is still alive, but the move was not uniform across the whole semiconductor complex.

The big picture remains the same: AI infrastructure is still the dominant equity theme, but the trade has become more selective. After the recent multiple expansion, that is healthy. We want the best companies to keep working, but we do not want everything with an AI label trading like fundamentals no longer matter.

Options

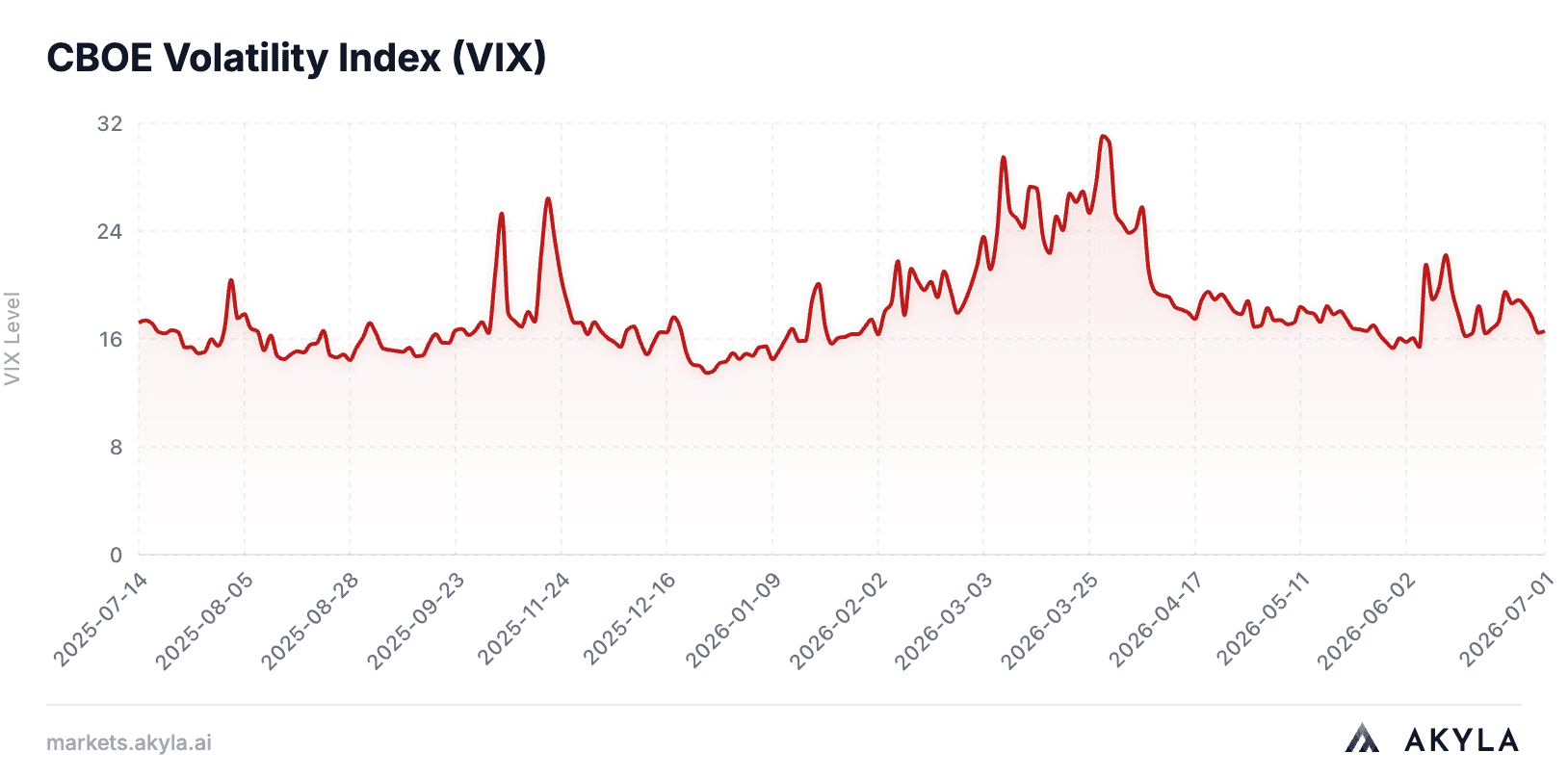

Options markets look calm.

VIX closed at 15.03, down 5.1% on the day. That is a meaningful signal. Despite the Iran headlines, hawkish Fed commentary, and elevated Treasury yields, investors are not aggressively buying downside protection.

A VIX around 15 is not consistent with panic. It is consistent with a market that sees risks, but still believes those risks are manageable.

That does not mean downside is impossible. It just means the options market is not currently pricing a major stress event.

Rates & Spreads

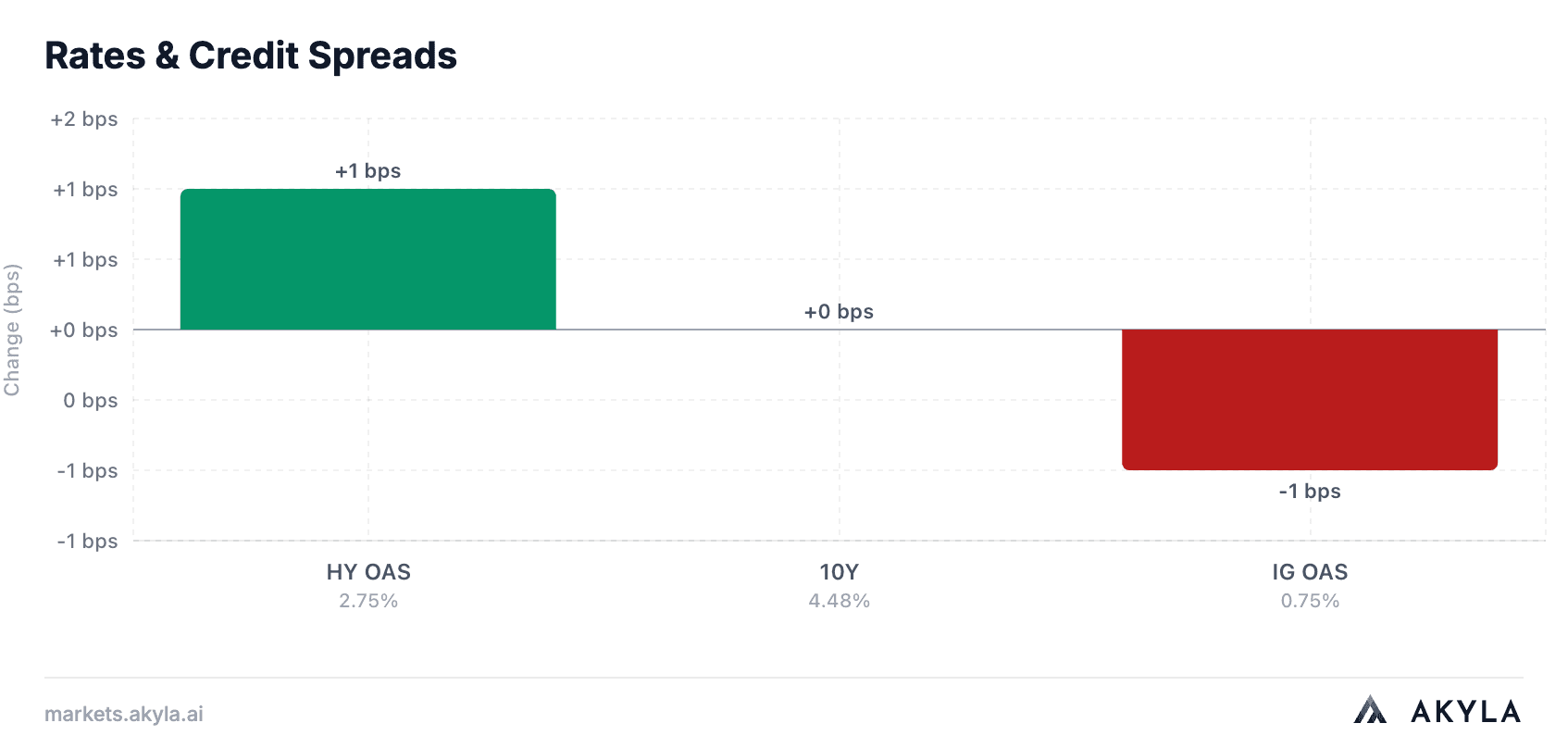

Credit still looks fine and is flat with minimal movement.

High-yield spreads remain at 2.75%, unchanged from the prior day and still comfortably tight. This is the chart that matters more than junk bond yields alone. If junk yields rise because Treasury yields rise, that is a rates move. If high-yield spreads widen, that is a credit-risk move.

For now, the credit market is not confirming the bear case.

This remains one of the most important reasons I am not overly worried about the equity pullback. If equities were falling, VIX was spiking, and high-yield spreads were widening, that would be a different story. But that is not what we have.

Commodities

Oil gave the market some relief.

WTI crude fell roughly 0.9% to $71.41, even though Iran-related risk remains in the background. That matters because the market’s biggest macro fear is not the war itself. It is the possibility that the war pushes energy prices high enough to reignite inflation and force the Fed into more tightening.

So far, oil is not confirming that worst-case scenario.

That is why I keep focusing on the YTD oil chart rather than the one-day headline. A 4% move sounds dramatic in isolation. But the real question is whether oil is breaking out in a way that changes inflation, margins, or consumer spending. Right now, the answer still looks like no.

Macro

The main macro update was the Fed’s July Monetary Policy Report. The report reinforced the current setup: inflation is still above target, growth remains moderate, the labor market is stable, and the Fed is not ready to give the market an easy dovish pivot. Reuters summarized the report as highlighting inflation pressure from tariffs, the Iran war, and AI-related investment, while noting that unemployment remains stable around 4.2%.

Rates are still restrictive. The Fed’s July 10 H.15 release showed the effective fed funds rate at 3.62%, the 10-year Treasury at 4.54%, and the 30-year Treasury at 5.05% as of July 9.

That is the main constraint on the market. Equities can keep working if earnings and AI capex remain strong, but elevated long-end yields limit how much multiple expansion investors should expect.

The takeaway: the macro backdrop is not great, but it is also not breaking. Inflation is still too high, the Fed remains hawkish, and yields remain elevated. But credit is calm, volatility is low, oil is contained, and equities are still absorbing bad headlines reasonably well.

For now, that is a healthy market.

For informational purposes only — not investment advice.