The asset sale will leave shareholders with cash and a retained ifetroban pipeline with positive Phase II results

TLDR

Cumberland Pharmaceuticals, CPIX -3.62%↓ , has an ~100 million in upfront cash — while retaining its ifetroban pipeline.

Overview

You read that right: an 100 mln cash. The setup looks unusually clean for a microcap pharma special situation. It’s too small for mid-sized funds to buy so it’s being overlooked.

Transaction History

On April 23, Cumberland announced a Strategic Transaction with Apotex Inc., the largest Canadian-based pharmaceutical company, to integrate the branded U.S. commercial businesses. Under the terms of the agreement, Apotex will acquire Cumberland's portfolio of FDA-approved brands for $100 million in cash consideration, subject to Cumberland shareholders' approval and certain other customary closing conditions (source).

Cumberland ran a competitive process involving both Apotex and “Investor A,” which helps reduce transaction risk because Apotex was not the only credible buyer at the table. Investor A had previously offered up to 90 million of upfront cash and a 100 million of upfront cash with no contingent component. The presence of a competing offer gives the Board a market-check data point and supports the view that the final Apotex transaction was negotiated against a real alternative.

Deal Structure

The transaction is structured as an asset purchase in which Apotex will acquire Cumberland’s commercial product assets, including rights to products such as Kristalose, Sancuso, Vibativ, Caldolor, Acetadote, Vaprisol, Omeclamox-Pak, and Talicia. The core consideration is $100 million in upfront cash on a cash-free, debt-free basis, with no financing contingency, which compares favorably to earlier proposals that included larger deferred or contingent components.

Cumberland also negotiated additional economic sweeteners, including a potential HHS/Vibativ milestone and an inventory-related covenant under which Apotex would pay an aggregate amount equal to no less than $9 million for inventory sold during the twelve months after closing. This makes the deal meaningfully cleaner than the prior earnout-heavy versions because the headline value is largely upfront cash, with upside through negotiated add-ons (page 57).

Next Steps (as of May 27th)

-

June 24, 2026

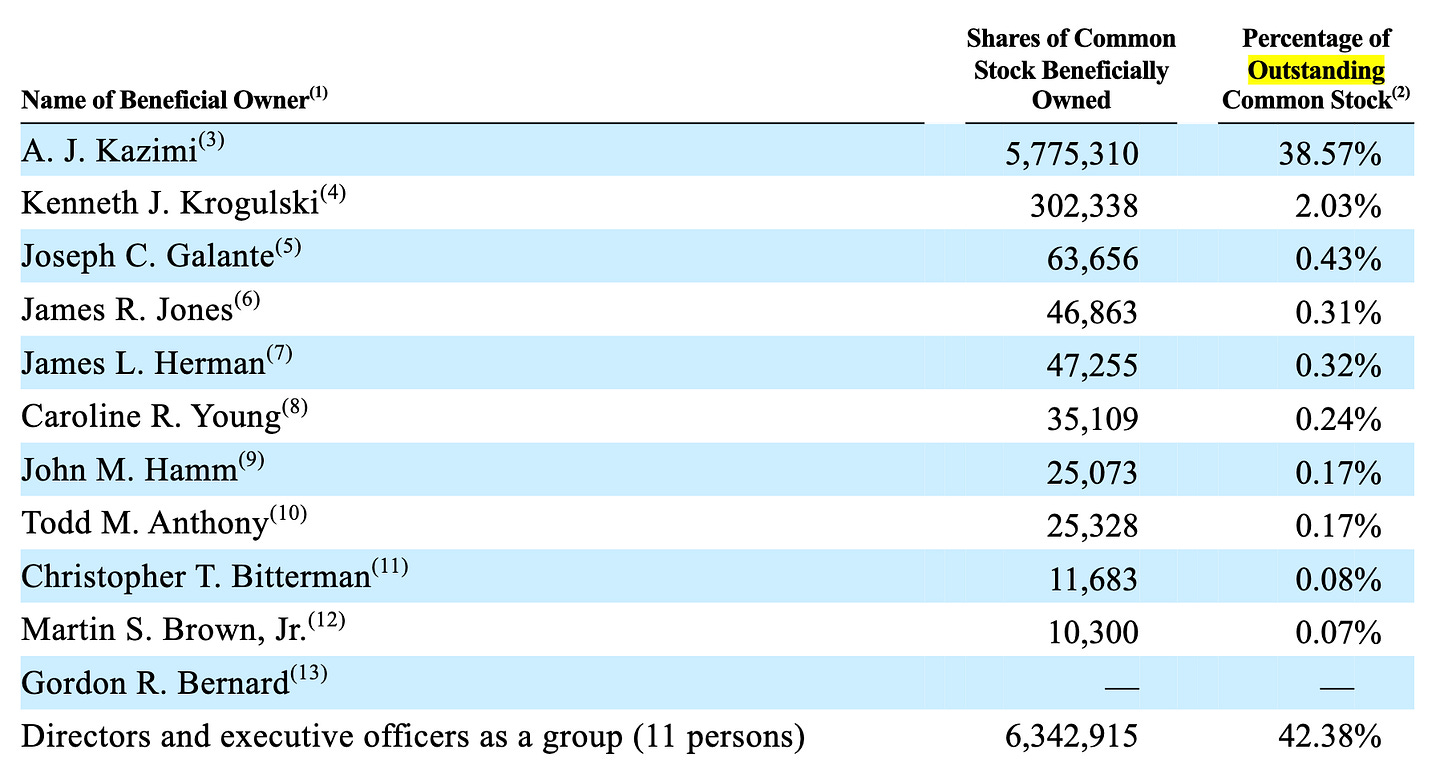

- Shareholders will be asked to approve the transaction - insiders control 42% of the company - see screenshot below

- Shareholders will be asked to approve the transaction - insiders control 42% of the company - see screenshot below

-

Q2 or Q3 closing

- To be determined, additional details to follow

What happens to Cumberland after the acquisition?

“The Company will retain the assets associated with its ifetroban product candidates and Cumberland Emerging Technologies, our majority-owned subsidiary focused on earlier-stage product development, which the Company intends to continue to develop following the closing of the transaction.” (letter from CEO dated May 26, 2026)

Cumberland will retain ifetroban and effectively become a clinical-stage development company focused on that asset. Ifetroban has been tested in over 1,400 subjects and has shown a favorable safety profile. The lead program is DMD-associated cardiomyopathy, where Phase II results showed improved heart function and the drug has received Orphan Drug, Rare Pediatric Drug, and Fast Track designations. The systemic sclerosis and idiopathic pulmonary fibrosis programs provide additional upside, though they appear less advanced than DMD. The go-forward business is therefore centered on using deal proceeds to advance ifetroban, with DMD as the main value driver and CET as an earlier-stage pipeline supplement.

Quick side note

The 14A notes in several places that “Based on Cumberland’s approximately 14.96 million shares of common stock then outstanding, the 6.68”. To arrive at that number, all they did was divide 6.68. That’s very dirty back of the envelope math. The ifetroban pipeline has value. A management team with experience closing deals (e.g. this 6.68 is still a 15% premium to today’s price of $5.77.

Conclusion

Cumberland is a small-cap special situation with an unusually simple setup: the company is selling its commercial assets for 88 million. If the deal closes, shareholders should be left with a cleaner balance sheet, retained ifetroban upside, and a more focused clinical-stage company. The key risk is execution: the transaction still requires shareholder approval and satisfaction of closing conditions. But with insider support, a competitive process, an all-cash structure, and a buyer with no financing contingency, the risk/reward looks unusually favorable for a situation this small. This is exactly the kind of overlooked microcap setup that can exist because it is too small for most institutions to bother with.

For informational purposes only — not investment advice.